July 2017

The Honourable Dave Levac, MPP

Speaker of the Legislative Assembly of Ontario

Main Legislative Building, Room 180

Queen’s Park

Toronto, Ontario

M7A 1A2

Dear Mr. Speaker:

In accordance with section 14 of the Financial Accountability Officer Act, 2013, I am pleased to present the 2016-17 Annual Report of the Financial Accountability Officer for your submission to the Legislative Assembly at the earliest reasonable opportunity.

Sincerely,

Stephen LeClair

Stephen LeClair

Financial Accountability Officer

Executive summary

The Financial Accountability Officer is an independent officer of the Legislative Assembly of Ontario. His role is to provide the Assembly with the economic and financial analysis it needs to perform its constitutional functions, especially scrutinizing the government’s fiscal plan and its implementation over the course of the fiscal year.

Mandate and activities

The FAO performs his role by providing the Assembly with analysis conducted on his own initiative and by responding to research requests from MPPs and the committees on which they serve.

In 2016-17, the FAO published four reports resulting from analytical projects he initiated: the Economic and Fiscal Outlook: Assessing Ontario’s Medium-term Prospects in spring 2016 and its fall 2016 update; Cap and Trade: Assessment of the Fiscal Impact of Cap and Trade; and Ontario Health Sector: Expense Trends and Medium-Term Outlook Analysis.

In 2016-17, the FAO received four formal research requests from MPPs; the FAO has not yet received a research request from a standing or select committee.

The FAO continues to meet with MPPs, both individually and collectively, to more fully appreciate their concerns, interests and needs and to better understand how their needs can best be met. The FAO would be pleased to appear before a committee to discuss a potential research request.

Access to information

In 2016-17, the FAO made 29 information requests of ministries and public entities. As of July 2017, all but one of these requests have been fulfilled.

In October 2016, the Lieutenant Governor in Council made an order-in-council, which requires ministries and public entities to provide the FAO with access to information contained in certain Cabinet records. The order-in-council, combined with ministries and public entities’ improved understanding of their duty to provide the FAO with information, has improved the FAO’s access to information necessary for the performance of the FAO’s duties.

The FAO looks forward to continuing to work with the public service to further improve the process for accessing information and more specifically, to ensure that ministries and public entities provide information in a timely manner.

Disclosure of information

As the FAO’s access to information has increased, the restrictions on the FAO’s disclosure of that information have taken on greater importance.

It is often challenging for the FAO to determine whether a specific restriction applies to information provided by ministries and public entities, so the FAO asks for their assistance in doing so.

The FAO plans to continue working with the public service to ensure that ministries and public entities provide the FAO with advice he needs to comply with the disclosure restrictions.

Independence

The Financial Accountability Officer (FAO) and his staff must be independent from influence by the government of the day in order to provide the Legislative Assembly with the impartial analysis it needs to perform its constitutional functions.

The FAO and his staff must also have sufficient education and experience to ensure that their work is credible and professional. Several provisions of the Financial Accountability Officer Act, 2013 (the FAO Act) work in concert to bolster and protect the FAO’s independence, impartiality and professionalism.

Officer of the Assembly

The FAO is designated as an “officer of the Assembly” by section 2 of the FAO Act.

Appointment

The FAO is appointed under section 2 of the FAO Act by the Lieutenant Governor in Council on address of the Legislative Assembly. The proposed FAO must first be approved by an opposition-majority panel of three MPPs, chaired by the Speaker. This provision ensures that all recognized parties in the Legislative Assembly approve the FAO’s appointment.

Terms of service

The FAO serves for a fixed, five-year term by virtue of section 2 of the FAO Act and can be reappointed for one additional five-year term. The FAO can only be removed for cause on address of the Assembly. The FAO is also barred from holding any other employment that would conflict with the performance of his duties.

Salary, expenses, budget and staffing

According to sections 3, 5 and 8 of the FAO Act, the FAO’s salary and expenses, as well as budget and staffing levels for the office, are approved by the Legislative Assembly’s Board of Internal Economy.

Qualifications of staff

Under section 8 of the FAO Act, the FAO has the power to hire staff for the office. The FAO has staffed the office with employees who have both experience and advanced education in economics and/or finance. The FAO encourages employees to pursue professional development opportunities to continue to develop their expertise.

Since many of those with the requisite experience at the provincial level work in Ontario’s public service, the FAO hopes to pursue the development of a formal understanding with the Secretary of the Cabinet (and other deputy ministers, as appropriate) to allow for secondments and permanent moves from the public service to the FAO and vice versa.

Terms and conditions of employment

Under section 8 of the FAO Act, the FAO can set the terms and conditions of employment for staff. The FAO requires that staff not engage in other work that would interfere with their contribution to the FAO’s performance of his duties. As an independent officer of the Assembly, the FAO will establish a distinct code of conduct consistent with the Assembly’s own code. For the time being, the FAO requires that staff respect the Office of the Assembly’s code of conduct as a condition of their employment.

Immunity

Under section 17 of the FAO Act, the FAO and his employees enjoy immunity from proceedings resulting from any action taken in the good faith performance of their duties.

Interference and obstruction

Section 18 of the FAO Act provides that the FAO can refer actual or attempted interference or obstruction of his work by an MPP or their staff, presumably including those employed in a minister’s office, to the Speaker of the Legislative Assembly. This provision was added while the bill creating the FAO was before the Standing Committee on the Legislative Assembly. Its express intention was to provide additional protection for the FAO’s independence.

If the FAO were to notify the Speaker under section 18, it would be up to all MPPs to determine how to respond to the notification. However, in light of the relevant precedents and authorities, the FAO expects that such a notification could result in an MPP raising a question of privilege.

Mandate and activities

The FAO has a three-part mandate under sections 10 and 11 of the FAO Act:

- Providing independent economic and financial analysis to the Legislative Assembly on his own initiative;

- Responding to requests for economic and financial research received from MPPs and committees; and

- Attending meetings of the Standing Committee on Finance and Economic Affairs and providing assistance at the committee’s request.

Whether on his own initiative or by request, the FAO can direct his office to examine both broad questions concerning the state of the Ontario government’s finances and the province’s economy, and more specific questions, including the economic and financial impact of the government’s budget, estimates and supplementary estimates, bills before the Assembly, and policy proposals that fall within the Legislature’s jurisdiction.

The flexible structure of the FAO’s mandate allows the FAO to use his professional judgment to bring significant economic and financial issues to the Legislative Assembly’s attention, while also meeting the more immediate needs of MPPs and committees by responding to research and assistance requests. The FAO looks forward to continuing to work with MPPs to ensure that they can easily engage with the FAO and his staff when they wish to make research requests or have other questions.

The FAO is mindful of the need to avoid overlap and duplication of work done by other officers of the Assembly, including the Auditor General and the Environmental Commissioner. The FAO coordinates with his fellow officers to ensure that he is providing the Assembly with timely and relevant economic and financial analysis.

Economic and financial analysis

In 2016-17, the FAO published four reports prepared on the FAO’s initiative. Two were regular reports on the state of Ontario’s economy and finances, and two were thematic reports on the impact that new or ongoing policy has on the province’s finances.

In May 2016, the FAO published the first spring Economic and Fiscal Outlook. Although the FAO’s short-term economic outlook presented in the report was broadly consistent with that presented in the 2016 budget, the fiscal outlook was not consistent with the one set out in the budget. The FAO identified several medium-term risks involving the possibility of weaker than expected economic growth, lower than anticipated revenues from cap and trade and federal transfers and higher than planned program spending due to demographic and cost pressures, particularly in the health sector.

In early November 2016, the FAO published the Economic and Fiscal Outlook Update. The FAO’s updated outlook incorporated information from the 2015-16 Public Accounts, proposed new spending commitments made in the Speech from the Throne and a revised economic outlook. In addition, the update incorporated a change in the accounting treatment for certain public sector pension plans. As a result of these changes, the FAO projected a significant deterioration in Ontario budget deficits in the coming fiscal years without additional measures to raise revenue or reduce expense.

In late November 2016, the FAO published An Assessment of the Fiscal Impact of Cap and Trade. The report analyzed the potential fiscal impact of cap and trade and showed that there would be an impact on the Province’s surplus or deficit if the Province:

- Used the funds to finance capital projects or programs that are already planned, then cap and trade expenses would be lower than revenues, resulting in a reduction in the deficit/increase in the surplus;

- Committed to spending that is difficult to reduce or stop, and revenues are lower than anticipated, then the deficit could be increased or surplus reduced; and

- Did not spend all of the cash raised from cap and trade in the same year, then it could reduce the deficit (or increase the surplus) in that year and increase the deficit (or reduce the surplus) in future years.

In January 2017, the FAO published a report on the Ontario Health Sector: Expense Trends and Medium Term-Outlook which reviewed how the province planned to achieve the health sector expense targets in the 2016 budget, and whether the low growth rate required to achieve those targets would be sustainable after 2018-19. The report noted that the annual growth rate of health sector expense had been reduced to around 2 per cent, largely by slowing growth in spending on hospitals and the Ontario Health Insurance Program. Key program changes since 2012 included a four-year freeze in base operating funding for hospitals and reductions in physician payment rates in 2013 and 2015. However, the FAO’s forecast for health sector expense, reflecting the program changes implemented by the province to date and maintained through to 2018-19, showed that additional program changes totalling expense savings of approximately $400 million in 2016-17, $900 million in 2017-18 and $1.5 billion in 2018-19 were required for the province to meet its health sector expense targets set out in the 2016 budget. Finally, after 2018-19, if those targets were achieved, then health sector expense would have averaged 2.1 per cent annual growth over seven years. The FAO’s review of health sector expense growth rate trends and cost drivers raised questions about the sustainability of 2.1 per cent annual growth, assuming that health care quality and service levels will be maintained.

The FAO also publishes backgrounders and commentaries. Backgrounders provide MPPs with short analyses of economic and financial issues. In 2016-17, the office published two backgrounders, one on the Province’s credit rating and the other on service fees. Commentaries examine economic and fiscal developments, such as major data releases, and provide MPPs with insights on the broader implications for the province’s economy and the government’s fiscal plan. In 2016-17, the office published 11 commentaries, including ones on provincial cash flows and debt, energy costs, the labour market, Ontario exports, postsecondary education spending and the fiscal impact of a potential housing market correction.

Economic and financial research requests

The FAO receives and considers research requests from MPPs and committees confidentially. The requests can relate to trends in the provincial and national economies, the state of the province’s finances, the estimates and supplementary estimates and/or the financial impact of a bill or other policy proposal.

The FAO has the discretion to refuse research requests under subsection 10(2) of the FAO Act. The FAO has released principles, which are based on Canadian and international best practices, which will guide his decision to accept or refuse a research request. These principles are available on the FAO’s website.

When the FAO accepts a research request from an MPP or a committee, the FAO will determine terms of reference in consultation with the MPP or the committee. The FAO will not reveal the identity of the requesting committee or MPP. The committee or the MPP will, however, be free to identify themselves as the requester of the research.

In 2016-17, the FAO received four formal research requests from MPPs and none from committees. The FAO welcomes requests from both MPPs and committees and would be pleased to appear before a committee to discuss a possible research request.

The FAO is also pleased to provide informal assistance to MPPs on questions regarding economic and financial matters. In some cases, those requests may result in formal reports, while in other cases, the FAO and his staff may be able to suggest existing reports or other resources that would respond to the question.

Assistance to the Standing Committee on Finance and Economic Affairs

The FAO anticipates that the Standing Committee on Finance and Economic Affairs may request his assistance in its pre-budget consultations and consideration of budget implementation bills or other bills that fall within its remit, as well as any substantive inquiries that the committee might choose to undertake.[1] The FAO looks forward to continuing to work with the committee to identify how the FAO and his office can best offer assistance.

The FAO would be pleased to assist other committees when they are considering legislation or conducting substantive inquiries into issues that relate to the FAO’s mandate. The FAO may also request to appear before committees considering bills or conducting inquiries that are related to his mandate.

Supporting the Legislative Assembly

In his first annual report, the FAO explored the origins of his office and identified some of the concerns that motivated its creation, concluding that the FAO’s role is to assist the Legislative Assembly in performing its constitutional functions when it comes to public money. In an effort to better appreciate how the FAO can fulfill that role and serve all members of the Assembly, the FAO hopes to periodically discuss related matters in his annual reports to the Assembly.

In the 2015-16 annual report, the FAO focused on the Assembly’s lack of access, whether directly or through its officers, to the full range of information it needs to perform those constitutional functions. The FAO recommended that the Assembly consider launching a review of the scope of the government’s disclosure over the course of the parliamentary financial cycle, and the degree to which the disclosure meets MPPs’ needs at various stages in that cycle. The FAO continues to believe that such a review would be useful and the FAO would be pleased to assist.

This year, the FAO wishes to more closely examine the way in which the Assembly performs its three major constitutional functions when it comes to public money and in particular, how it might evolve to better allow individual MPPs and the committees on which they serve to conduct financial scrutiny.

The Assembly approves the government’s plans to raise and spend money.

The Assembly approves the government’s fiscal plan by voting on a motion that “approves in general the budgetary policy of the government” set out in the budget and by concurring in the government’s main estimates.[2] The Assembly must also concur in any supplementary estimates required over the course of the fiscal year to meet unexpected expenditures and fund new programs.[3]

The Assembly cannot, however, substitute its own preferences about how to raise money or what to spend it on for those of the government.[4] If the Assembly does not approve the government’s fiscal plan, the government is expected to resign or ask the Lieutenant Governor to dissolve the Legislature for a general election.

The Assembly implements the government’s fiscal plan by passing the necessary money bills.

Budget implementation bills make any necessary changes to the tax system and other budget-related changes to provincial laws. There are usually two budget implementation bills, one following the budget in the spring and one following the Economic Outlook and Fiscal Review in the fall.[5] The spring budget implementation bill generally authorizes the government to borrow money.[6]

Although part of the province’s spending is authorized by permanent legislation, annual supply bills appropriate much of the money that ministries need to fund the various specific programs they operate.[7] There is usually one main supply bill a year, which corresponds to the estimates concurred in by the Assembly.[8] Since the Assembly does not pass the main supply bill until after the beginning of the fiscal year, the Assembly can pass a motion for interim supply for up to six months.[9] The Assembly has, in recent years, passed an interim supply bill in the fall.[10] Likewise, the Assembly often passes supplementary supply bill in the fall, which corresponds to the supplementary estimates.[11]

Once the Assembly passes the bills, the Lieutenant Governor gives the bills royal assent and they are enacted into law.

The Assembly studies the government’s fiscal plan and associated money bills when they are before the Assembly, and scrutinizes the government’s efforts to implement them over the course of the fiscal year.

The Assembly performs most of its scrutiny activities through its standing committees.

The Assembly’s scrutiny effectively begins before the start of the fiscal year with the Standing Committee on Finance and Economic Affairs’ pre-budget consultations. Although the pre-budget consultations are intended to inform the budget, they can also help create a benchmark that MPPs can use to evaluate the government’s fiscal plan and its implementation. If consultations indicate that a certain economic or financial issue is of particular concern to Ontarians and that issue is not addressed in the fiscal plan, MPPs can ask the government to justify its decision not to tackle the issue.

The Assembly scrutinizes the fiscal plan through the Standing Committee on Estimates, which selects certain ministries’ estimates for study. Both the government and opposition parties get to choose up to four ministries and offices each whose estimates will be considered by the Standing Committee on Estimates.[12] In contrast to most other standing committees, the Standing Committee on Estimates regularly calls ministers to testify on their ministries’ programs. The Standing Committee on Estimates is chaired by an opposition MPP, which increases its independence from government.[13]

The Assembly scrutinizes the implementation of the fiscal plan on an ongoing basis through the Standing Committee on Public Accounts, which takes up the Auditor General’s reports and examines the public accounts.[14] The Standing Committee on Public Accounts regularly calls senior ministry officials to testify on their ministries’ activities. The Standing Committee on Public Accounts is chaired by an MPP who is a member of the official opposition.[15]

The Assembly can also scrutinize the fiscal plan by referring budget implementation and other bills to committee for study. (Since main supply bills implement the estimates, they are not separately studied in committee.) The Standing Committee on Finance and Economic Affairs generally studies budget implementation bills. The Standing Committee on Finance and Economic Affairs, like most standing committees, does not call the Minister of Finance or his senior officials to testify on budget implementation bills. Those bills often make complex changes to tax and other financial legislation and the House of Commons’ experience suggests that testimony by Ministers and officials can be helpful in helping members understand and scrutinize those changes.

The Assembly could also do so by calling ministers and public servants to testify before committees on their ministries and the programs they operate. The Standing Committees on Justice Policy, Social Policy and General Government are empowered to study “all matters related to the mandate, management, organization or operation of the ministries…assigned to them”.[16] These policy field committees rarely undertake general studies of the ministries that fall under their mandate. This is true even for the ministries with the largest budgets, such as the Ministry of Health and Long-Term Care, Education and Advanced Education and Skills. Although such studies would not deal directly with the ministries’ estimates, they could provide MPPs with an opportunity to scrutinize the ministries’ policy and operational decisions, which are often made because of financial considerations and may have an impact on the government’s ability to fulfill its fiscal plan.

Renewing Assembly’s scrutiny

When a government enjoys the support of a disciplined majority in the Assembly, as is currently the case, the adoption of its fiscal plan and its implementation through the necessary legislation is nearly a foregone conclusion. By contrast, a minority government must negotiate with opposition caucuses to secure their support for its plans and thereby ensure that it can remain in office.

No matter the composition of the Assembly, all of its members who are not serving as ministers, whether they are sitting in the government or opposition benches, are responsible for scrutinizing the government’s plans over the course of the fiscal year. As Standing Order 1 makes clear, MPPs enjoy the “democratic right” to “hold the government to account for its policies.”

Financial scrutiny is a challenging and multi-faceted task. The Assembly needs to ensure that the government has made a responsible fiscal plan, based on prudent economic and financial projections, and that the government updates it as needed in light of economic and financial developments. The Assembly has to examine the government’s major policy announcements and bills, as well as the activities of ministries and other public entities, over the course of the year to ensure that they are consistent with that plan. The Assembly must ultimately ensure that the government is respecting its will, raising and spending money only in the ways the Assembly has authorized.

These heavy tasks fall on the shoulders of backbench MPPs, both in the government and opposition parties. They face competing demands on their time, often lack access to useful information about economic and financial matters and historically had limited economic and financial analytical support.

As the FAO suggested in last year’s annual report, MPPs could review whether they have access to information, particularly in terms of the estimates and ministries’ briefing books, necessary to perform financial scrutiny. The FAO would be pleased to assist any committee charged with reviewing the information provided to the Assembly in support of its scrutiny function.

The FAO’s own role is to provide MPPs with economic and financial analysis, which in addition to the reports prepared by other officers of the Assembly, particularly the Auditor General, and the research provided by the Legislative Library and Research Services provides MPPs with the context necessary to perform effective scrutiny and helps them understand information provided by government. The FAO looks forward to working with MPPs to better understand how to support their scrutiny function.

Several scholars have suggested that the reduction of the Assembly from 130 to 103 MPPs in 1999 (increased to 107 MPPs in 2007) undermined the Assembly’s capacity to scrutinize government by reducing the number of backbench MPPs available to serve on committees and increasing the proportion of the government’s caucus serving in Cabinet.[17]

The result is that many MPPs serve on multiple committees, reducing the time that they can devote to their work on any one committee. Most government MPPs, including several committee chairs, also serve as parliamentary assistants to ministers, further reducing the time they have to devote to their committee duties.

Under the Representation Act, 2015, the Assembly will increase from 107 to 122 MPPs in 2018.[18] No matter the composition of the Assembly after the election scheduled for next June, the addition of 15 new MPPs represents an opportunity for the Assembly to consider whether it is using its existing procedures to effectively scrutinize the government’s fiscal plan and its implementation and whether those procedures should be reformed.

For instance, the 15 new MPPs could help reinvigorate the standing committees and particularly the policy field committees. Likewise, MPPs may wish to consider whether, as in other provincial legislative assemblies and the House of Commons, the responsibility for scrutinizing the estimates might be shared among multiple standing committees.

The FAO would be pleased to assist any committee tasked with reviewing the way in which the Assembly performs its constitutional functions when it comes to public money, particularly financial scrutiny. The FAO very much looks forward to continuing to work with all MPPs on these matters.

Access to information

The FAO’s ability to provide the Legislative Assembly with economic and financial analysis depends on the FAO’s access to information held by the Ontario government.

The Legislature recognized the importance of the FAO’s access to information, when in section 12 of the FAO Act, it imposed a clear duty on ministries and other public entities to provide the FAO with any information that he requests and considers necessary for the performance of his duties. In the debates on the creation of the FAO, MPPs were clear in their determination that the FAO would have access to all the information needed to perform his duties.

While the bill that created the FAO was before the Assembly, the Standing Committee on the Legislative Assembly made several changes to the bill to bolster the FAO’s access to information. Most of those changes were supported by MPPs from all three parties represented in the Assembly. The Standing Committee sought to ensure that the exceptions to ministries’ and public entities’ duty to provide the FAO information would be specific and limited, and that the FAO would have access to a parliamentary remedy if denied access to information.

The FAO continues to work with the Ontario public service to ensure that the FAO can access all the information he needs to provide timely and relevant analysis to the Assembly. In October 2016, the Lieutenant Governor in Council made an order instructing ministries and public entities to provide the FAO with information contained in certain Cabinet records, narrowing the scope of the Cabinet records exception. Since the order-in-council was made, the FAO has been able to access more information than he could before, particularly when it comes to detailed medium-term spending projections.

The FAO has prepared a guide to assist ministries and public entities in responding to information requests. The guide, which was last updated in January 2017, is available on the FAO’s website.

Information requests

In 2016-17, the FAO made 29 formal information requests in support of 10 analytical projects.

These requests, which usually contain several specific questions, take the form of official correspondence between the FAO and the deputy minister of the ministry (or equivalent in the case of public entities) from which the FAO is requesting the information. The FAO makes information requests and responses available on the FAO’s website.

Of the 29 information requests made by the FAO, 28 were fulfilled and one was partially fulfilled. The partially fulfilled information request was submitted before the Lieutenant Governor in Council made the order granting the FAO access to information contained in certain Cabinet records. The project to which that request related was discontinued.

In their responses to requests made after the order-in-council came into force, several ministries explained that they were unable to provide some requested information before certain Cabinet decisions were announced in the budget. After the 2017 budget was introduced, the FAO asked those ministries to provide the remaining information, which they did.

Compared to 2015-16, ministries and public entities have fulfilled a larger proportion of the FAO’s information requests. The improvement in ministries and public entities’ compliance can be partly explained by the order-in-council granting the FAO access to information contained in certain Cabinet records and partly by ministries and public entities’ improved understanding of the FAO’s mandate and access to information.

Accessing information in a “timely manner”

The FAO’s information requests generally include deadlines and the FAO will not refuse ministries and public entities’ requests for reasonable extensions. But the FAO is concerned that some ministries and public entities do not always provide information in the “timely manner” required by subsection 12(1) of the FAO Act.

The FAO provides the Legislative Assembly with economic and financial analysis in support of the Assembly’s performance of its constitutional duties. Because the Assembly performs those duties according to a predetermined schedule and often on short timelines, the FAO aims to provide MPPs with relevant analysis in a timely manner. Without timely access to government information, it is more difficult for the FAO to provide timely and comprehensive analysis to the Assembly.

The FAO expects that as ministries and public entities come to better understand their duty to provide the FAO with information, they will be able to provide information more promptly. The FAO plans to report on timeliness of responses to information requests in future annual reports.

Exceptions to ministries’ duty to provide information

There are only three, limited exceptions to the FAO’s power to access information from ministries and public entities. Only one – the Cabinet records exception – has so far been relied upon by ministries and public entities in their responses to the FAO’s information requests.

Cabinet records exception

Subsection 12(2) of the FAO Act provides that the FAO cannot access Cabinet records as defined under section 12 of the Freedom of Information and Protection of Privacy Act (FIPPA).[19]

Generally, a Cabinet record is one whose disclosure “would reveal the substance of deliberations of the Executive Council or its committees.”[20] There are specific categories of documents that are also designated as Cabinet records by paragraphs 12(1)(a) through (f) of FIPPA. Some of the categories serve to protect the positions taken by ministers before and during Cabinet deliberations. Others serve to protect the integrity of the Cabinet decision-making process by ensuring that the materials under deliberation are not released before Cabinet has had a chance to consider them.

The Information and Privacy Commissioner and to some extent, the courts (which review the Commissioner’s decisions) have interpreted section 12 of FIPPA. Since the definition of “Cabinet records” from FIPPA is incorporated into the FAO Act, the FAO and the ministries and public entities from which he requests information are guided by the Commissioner’s interpretations of FIPPA.

The Information and Privacy Commissioner has broadly interpreted the general definition of Cabinet records set out in subsection 12(1) of FIPPA. The Commissioner has held that a record would reveal the substance of Cabinet deliberations if it allows the drawing of accurate inferences about the substance of those deliberations.[21] Likewise, the Commissioner has concluded that a record that has not been put before Cabinet can still be considered a Cabinet record if there is a sufficient connection between its contents and the actual substance of Cabinet deliberations.[22]

Limitations on exception

Despite its broad scope, the Cabinet records exception is subject to several limitations:

- the exception is time-limited under paragraph 12(1)(c) of FIPPA because it does not apply to “background explanations or analyses of problems” once the decisions to which they relate have been “made and implemented” and under paragraph 12(2)(a) of FIPPA because it does not apply to any other records that are more than 20 years old;

- the exception does not apply if Cabinet consents to the release of information under paragraph 12(2)(b) of FIPPA;

- ministries and public entities must provide the FAO with any information that can be severed from what would otherwise be a Cabinet record; and

- the exception does not apply to information that might otherwise be considered a Cabinet record but is made publicly available by statute or under the Standing Orders of the Legislative Assembly.[23]

Order-in-council on Cabinet records

In the 2015-16 annual report, the FAO raised concerns about ministries’ apparent overuse of the Cabinet records exception. In particular, in their responses to the FAO’s information requests, several ministries asserted that the Cabinet records exception prevented them from providing the FAO with information about the Ontario government’s revenue and spending projections for future fiscal years. The FAO was created in part to provide the Legislative Assembly with independent analysis of such projections. Without access to them, the FAO cannot fully perform his mandate.

Following the tabling of the 2015-16 annual report, the FAO entered into discussions with the government and public service about how the Cabinet records exception could be narrowed to allow the FAO to access the information necessary to perform his mandate while continuing to protect the confidentiality of the actual deliberations of Cabinet and its committees.

As a result of those discussions, the Lieutenant Governor in Council made an order-in-council consenting to the FAO having access to information contained in certain Cabinet records under subsection 12(2) of the FAO Act.[24]

The order-in-council requires ministries and public entities to provide the FAO with economic, financial or other information contained in a Cabinet record, subject to several conditions:

- The information relates to an aspect of the FAO’s mandate;

- The information is not available from another source;

- The Cabinet decision to which the information relates has been made and publicly announced, even if Cabinet or one of its committees may engage in further deliberation on the decision;

- The information can be provided in a form that does not reveal other information that is either not relevant to the FAO’s mandate, including communications materials, or needs to be protected to maintain the confidentiality of actual Cabinet deliberations, including information relating to the individual opinions of Cabinet ministers;

- The information does not reveal personal information or personal health information as defined in subsection 12(3) of the FAO Act.

The order-in-council applies to all Cabinet records prepared in respect of Premier Kathleen Wynne’s government. The order-in-council does not, however, apply to records prepared in respect of past governments in the past 20 years.

It will not apply to records that will be prepared in respect of future governments. Paragraph 12(2)(b) of FIPPA, which is incorporated into subsection 12(2) of the FAO Act, does not allow a Cabinet to consent to the disclosure of records related to a past or future Cabinet. By contrast, the three orders-in-council that authorize the federal Auditor General’s access to Cabinet confidences apply to the confidences of the government that approves them and all future governments.[25]

The FAO will continue to work with the government and the legislature to ensure that the FAO continues to have access to the information necessary to perform the FAO’s mandate.

Personal information and personal health information exception

Under subsection 12(3) of the FAO Act, the FAO also cannot access personal information and personal health information, which are defined in the Freedom of Information and Protection of Privacy Act and the Personal Health Information Protection Act, 2004, respectively. The exception covers various kinds of information that would allow someone to identify the person to whom the information relates.

When considering the bill that created the FAO, the Standing Committee on the Legislative Assembly added subsection 12(4) of the FAO Act, which requires ministries to redact personal information and personal health information from the information they provide to the FAO. The express intention of this amendment was to maximize the amount of information that ministries and public entities can provide to the FAO.

Hydro One exception

A third exception to the FAO’s power to access information set out in subsection 16.1(1) of the FAO Act prevents the FAO from accessing information held by Hydro One and its subsidiaries, which are not considered public entities for the purposes of the FAO Act.

Remedy for failure to comply with an information request

Subsection 12(5) of the FAO Act provides that the FAO can notify the Speaker of the Legislative Assembly and the chair of the Standing Committee on Finance and Economic Affairs if he is of the opinion that a ministry or public entity has failed to comply with an information request. This provision was added when the bill creating the FAO was before the Standing Committee on the Legislative Assembly and reflects MPPs’ determination that the FAO have access to all information necessary to perform his duties.

The order-in-council granting the FAO access to certain Cabinet records does not affect the FAO’s power to notify the Speaker and the chair of the Standing Committee on Finance and Economic Affairs of a refusal to comply with an information request.

The FAO is prepared to notify the Speaker and committee chair if a ministry or public entity fails to provide information in a timely manner; improperly invokes one of the exceptions under the FAO Act or the order-in-council; or claims that it cannot provide information for any other reason.

If the FAO were to notify the Speaker and committee chair, it would be up to all MPPs to decide how to respond to the notification. However, in light of the precedents, especially the Speaker’s ruling concerning the Information and Privacy Commissioner’s 2000 report on the former Province of Ontario Savings Office, the FAO expects that such a notification could result in an MPP raising a question of privilege.[26]

Disclosure of information

The FAO has access to more government information than can be disclosed because he is subject to disclosure restrictions. These restrictions aim to protect various forms of sensitive information, particularly Cabinet confidential information and information originally provided to the government in confidence by another person or institution.

Under the Cabinet records order-in-council, the FAO cannot disclose information that originates in a Cabinet record, unless the FAO obtains the Executive Council’s consent.

Although, as was previously discussed, the order-in-council has helped increase the FAO’s access to information, the FAO cannot disclose the Cabinet confidential information he received under the terms of the order-in-council. Where analysis released by the FAO is based on Cabinet confidential information, the FAO may not be able to provide a detailed explanation of the specific information and methods which his staff used to reach conclusions presented in reports.

Under section 13 of the FAO Act, the FAO can disclose non-Cabinet confidential information provided by government only if certain conditions are met:

- The disclosure must be “essential” for the performance of the FAO’s duties.

- The information must not have been obtained solely from records that fall under certain categories of sensitive information defined by reference to the Freedom of Information and Protection of Privacy Act (FIPPA):

-

information whose disclosure would affect Ontario’s intergovernmental relations (section 15 of FIPPA);

-

information whose disclosure would affect the province’s economic and financial interests (subsection 18(1) of FIPPA); and

-

information which was provided to a third party or whose disclosure would cause harm to a third party (section 17 of FIPPA).

- The FAO and the ministries and public entities from which he requests information are guided by the Information and Privacy Commissioner’s interpretations of these FIPPA provisions.

The information must also not be subject to solicitor-client, litigation or settlement privilege.

- The FAO and the ministries and public entities are guided by the tests established at common law to determine whether information is subject to these privileges.

- The FAO can, however, disclose information that falls under sensitive categories or information protected by various legal privileges if the FAO obtains the consent of the appropriate person or institution.

The FAO does not generally disclose information in the original form provided by government and instead publishes economic and financial analysis based on that information and other publicly available information. Where some or all of the information supporting analysis released by the FAO is subject to disclosure restrictions under section 13 of the FAO Act, the FAO may not be able to provide a detailed explanation of the specific information and methods which his staff used to reach conclusions presented in reports.

It can be difficult for the FAO to assess whether the information provided by a ministry or public entity falls under a sensitive category. That is especially the case if that category is defined in terms of the harm that would result from the disclosure of information. The FAO is often ill-placed to assess that potential harm. Likewise, if the FAO wishes to seek consent to disclosure, it could be difficult for the FAO to identify which person or institution must consent to the disclosure. For instance, it may not be clear that information provided by a ministry or public entity was originally provided by a third party or an institution which is neither a ministry nor a public entity.

As a result, the FAO asks ministries and public entities providing the FAO with information to identify information subject to disclosure restrictions. The FAO requests that ministries and public entities specifically identify the applicable restriction. The FAO uses the advice provided by ministries and public entities in the analytical and report writing process to ensure that reports are written in a way that does not disclose restricted information.

If the FAO provides a ministry or a public entity with a copy of a draft report for its review, the FAO also asks them to identify any information subject to disclosure restrictions and provide an explanation of why the restriction applies. Where the Information and Privacy Commissioner or the courts have established a test to determine whether a particular restriction applies, the FAO asks the ministry or public entity to show how each element of the test applies to the information in question.

If a ministry or public entity indicates that the draft report contains restricted information, the FAO will consider revising the report to remove the information. The FAO alone makes the final decision about what to report to the Legislative Assembly.

The FAO considers ministries and public entities’ assistance in this regard to be essential for complying with the disclosure restrictions set out in section 13 of the FAO Act and the order-in-council.

The FAO continues to work with the Ontario public service to ensure that the FAO has the information he needs to comply with the disclosure restrictions while providing timely and relevant economic and financial analysis to the Assembly.

Reporting

The FAO is an officer of the Legislative Assembly and the FAO’s role is to provide the Assembly as a whole with economic and financial analysis. For these reasons and to facilitate the Standing Committee on Finance and Economic Affairs’ review of the FAO’s reports under section 16 of the FAO Act, the FAO presents all reports that his office produces to the entire Assembly, even if the research presented in the report was originally requested by a particular committee or MPP.

As mentioned previously, the FAO publishes backgrounders and commentaries on the FAO’s website. Since the FAO is an officer of the Assembly and makes information requests on the Assembly’s behalf, the FAO will present the Assembly with an official, printed copy of any backgrounders and commentaries derived from information provided in response to information requests.

The FAO will continue to publish reports when the Assembly is prorogued, but not during the period from the day on which the legislature is dissolved for a general election until the end of the caretaker period. The FAO makes any reports he releases available on his website.

Section 15 of the FAO Act requires that the FAO deliver a copy of each report to the Minister of any ministry and the head of any public entity to which the report is relevant before the report is publicly released. Where necessary, the FAO will work with the Secretary of the Cabinet to identify which ministries and public entities are relevant to the content of a report.

Where appropriate, the FAO may also share draft reports with the relevant ministries and/or public entities for their comments. The FAO and his staff are grateful for the comments provided by ministries and public entities, as these comments have improved the final reports and helped the FAO better serve the needs of MPPs.

Accountability

The FAO is subject to several accountability mechanisms that serve to ensure that he is fulfilling the duties with which he has been charged by the Legislative Assembly and is exercising his powers responsibly.

The FAO’s annual reports, which summarize the work of the FAO’s office, are an important accountability tool. Annual reports, along with the FAO’s other reports, are automatically referred to the Standing Committee on Finance and Economic Affairs for their review and comments under section 16 of the FAO Act. The FAO also aims to keep the Standing Committee on Finance and Economic Affairs generally informed of his activities during the year.

The FAO would be pleased to appear before the Standing Committee on Finance and Economic Affairs to testify on any of his reports or any other matter. The FAO also welcomes any recommendations the committee might have to offer when it comes to the manner in which the FAO is performing his duties and exercising his powers.

The FAO plans to commission an external review of its work in the coming years. The review will be partly modelled on the external review of the United Kingdom’s Office of Budget Responsibility completed in September 2014. The recent review of Australia’s Parliamentary Budget Officer is also an important model because it combined an external review with parliamentary committee scrutiny. Along these lines, the FAO hopes that the Standing Committee on Finance and Economic Affairs will participate in the eventual review of the FAO’s work.

The FAO is also subject to financial and performance audits by the Auditor General under section 5 of the FAO Act. The FAO is also subject to the Public Sector Salary Disclosure Act, 1996, and discloses his own salary, as well as those of any staff paid more than $100,000 in accordance with that Act.

In accordance with the practices followed by other officers of the Assembly, the FAO will proactively disclose his expenses, as well as those of his senior staff, on a regular basis on his website.

Financial statement

The Board of Internal Economy approves the FAO’s budget and staffing levels under sections 5 and 8 of the FAO Act.

In early 2016, the FAO submitted a proposed budget for 2016-17 to the Board of Internal Economy, which approved it later that year. The FAO based the 2016-17 budget on the FAO’s operations in 2015-16, the FAO’s professional judgment and the Legislature’s intentions reflected in the FAO Act.

As 2016-17 was the office’s second year in operation, the office was not yet fully staffed and its operations and practices continued to evolve as the FAO sought to better serve the needs of MPPs.

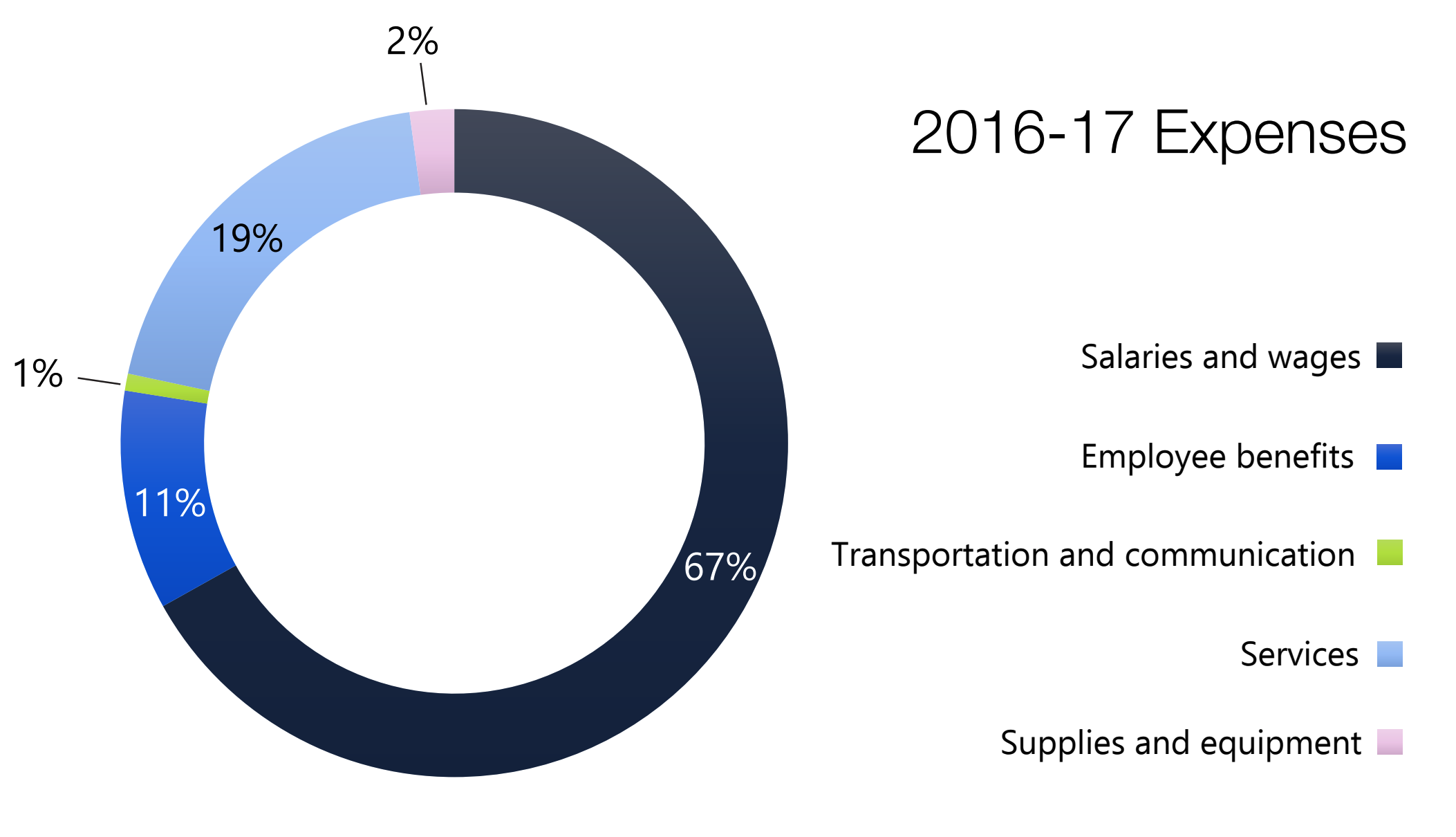

The FAO’s approved budget for 2016-17 was $3,255,000; the actual spending for the fiscal year was $2,615,186. The FAO spent less than expected because expenses for employees’ salaries and the preparation of reports for the Legislative Assembly were lower than anticipated.

Salaries, wages and benefits

The FAO’s approved staffing for 2016-17 was 20 full-time equivalent (FTE) positions. The FAO did not hire the full complement of staff as it continued to better assess the Assembly’s needs and develop its operations and practices accordingly.

At the end of the fiscal year, the office had 17.5 FTEs. Most employees worked full-time for the entire fiscal year with the exception of two students. Actual expenses for salary, wages and benefits in 2016-17 were $2,027,474.

Accessible version

| Salaries and wages | 67% |

|---|---|

| Employee benefits | 11% |

| Transportation and communication | 1% |

| Services | 19% |

| Supplies and equipment | 2% |

| 2016-17 Actual (Unaudited) |

2015-16 Actual27 (Audited) |

|

|---|---|---|

| Approved budget | $3,225,000 | $2,249,500 |

| Expense | ||

| Salaries and wages | $1,749,177 | $966,645 |

| Employee benefits | $278,298 | $184,756 |

| Transportation and communication | $21,441 | $39,732 |

| Services | $510,091 | $698,85428 |

| Supplies and equipment | $56,181 | $217,170 |

| Total | $2,615,186 | $2,107,157 |

Operating expenses

Services account for most of the FAO’s operating expenses. These include rent, translation and printing of reports, recruitment of employees, technical and professional support and one-time costs resulting from the acquisition and building out of the FAO’s office space. Actual expense for services in 2016-17 was $510,091.

The remainder of the FAO’s operating expenses were divided between $56,181 in actual expense for supplies and equipment and $21,441 for transportation and communication. The lower than expected supplies and equipment expense resulted from the FAO preparing fewer than the expected number of reports as the FAO continues to develop its operating model. The lower than expected transportation and communication expense reflects delays in staffing and less travel than expected.

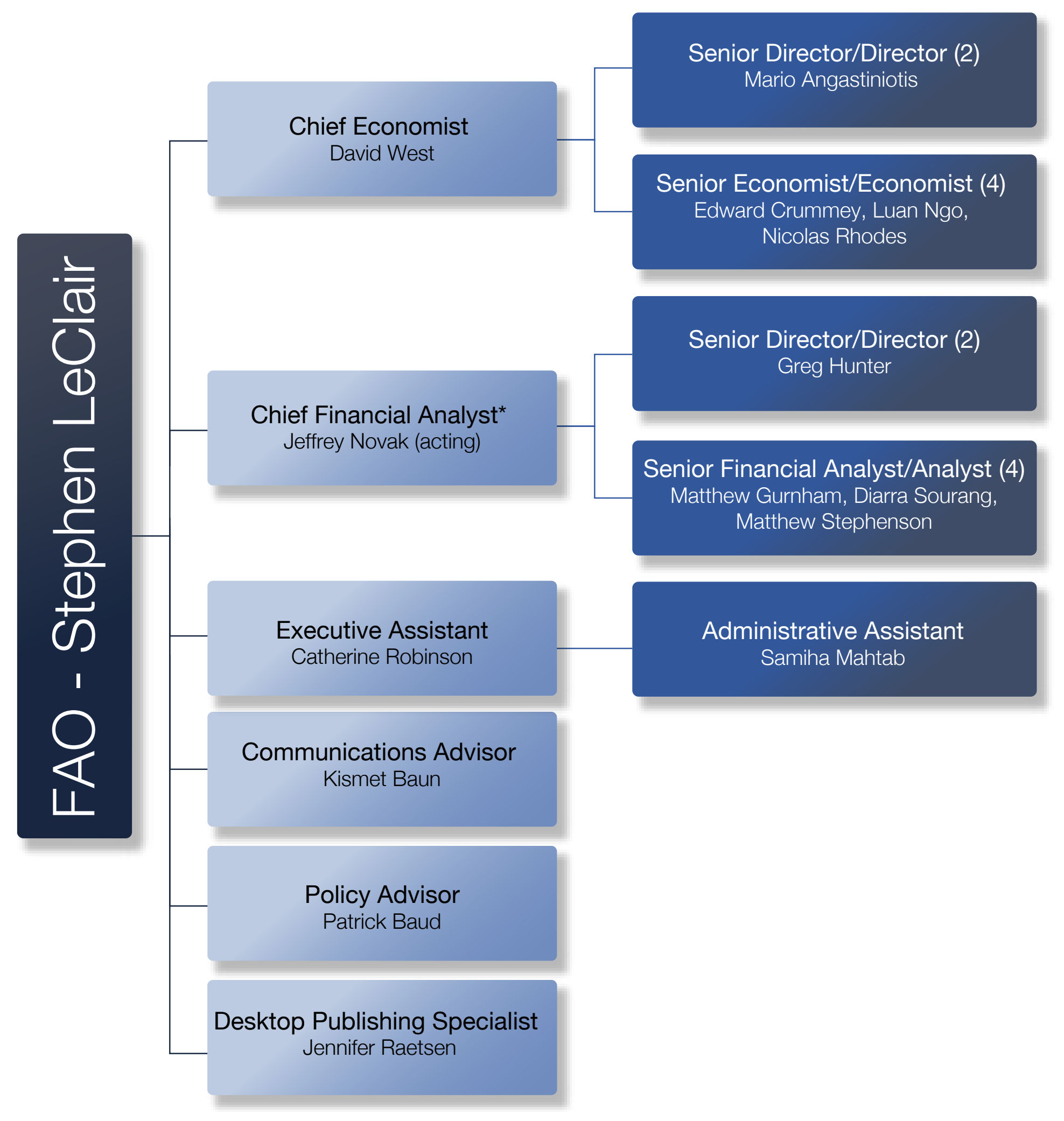

Office organization

Drawing on experience from other independent fiscal institutions (IFIs), the FAO operates as a relatively flat organization with limited hierarchy. This encourages greater staff flexibility and improves the efficiency of the FAO’s operations. In addition, drawing on best practices from other IFIs, the FAO focuses its resources on research and analysis, rather than internal processes and administration.

* Peter Harrison served as the FAO’s first Chief Financial Analyst from August 2015 to May 2017. Jeff Novak, Senior Director, Financial Analysis, was appointed Acting Chief Financial Analyst in May 2017.

Accessible version

- FAO – Stephen LeClair

- Chief Economist David West

- Senior Directore/Director (2) Mario Angastiniotis

- Senior Economist/Economist (4) Edward Crummey, Luan Ngo, Nicolas Rhodes

- Chief Financial Analyst* Jeff Novak (acting)

- Senior Director/Director (2) Greg Hunter

- Senior Financial Analyst/Analyst (4) Matthew Gurhan, Diarra Sourang, Matthew Stephenson

- Executive Assistant Catherine Robinson

- Administrative Assistant Samiha Mahtab

- Communications Advisor Kismet Baun

- Policy Advisor Patrick Baud

- Desktop Publishing Specialist Jennifer Raetsen

- Chief Economist David West

Appendix

Order in Council 1412/2016

https://www.ontario.ca/orders-in-council/oc-14122016

On the recommendation of the undersigned, the Lieutenant Governor of Ontario, by and with the advice and concurrence of the Executive Council of Ontario, orders that:

WHEREAS the Financial Accountability Officer, an Officer of the Legislative Assembly, was appointed to provide independent analysis to the Assembly about the state of the Province’s finances, including the budget, and trends in the provincial and national economies;

AND WHEREAS the Financial Accountability Officer requires access to information in the custody and control of Ministries and public entities in order to fulfill his statutory mandate;

AND WHEREAS certain information in the custody and control of Ministries and public entities is protected by the mandatory Cabinet Records exemption of section 12 of the Freedom of Information and Protection of Privacy Act;

AND WHEREAS the Lieutenant Governor in Council considers it advisable to provide the Financial Accountability Officer access to this information;

NOW THEREFORE Pursuant to subsection 12(2) of the Financial Accountability Officer Act (the “Act”) and subsection 12(2) paragraph (b) of the Freedom of Information and Protection of Privacy Act:

-

Every Ministry of the Government of Ontario and every public entity is authorized to provide to the Financial Accountability Officer any financial, economic or other information protected by section 12(1) of the Freedom of Information and Protection of Privacy Act that relates to:

- The Province’s finances, including the budget, and trends in the provincial and national economies

- The estimates and supplementary estimates submitted to the Legislature

- The financial costs or financial benefits to the Province of any public bill before the Assembly, or

- The financial costs or financial benefits to the Province of any proposal that relates to a matter over which the Legislature has jurisdiction, including any proposal made by the Government or by any member of the Assembly subject to paragraphs 2 and 3 below.

-

Information outlined in paragraph 1 above shall be provided to the Financial Accountability Officer in accordance with subsection 12(1) of the Act provided that:

- The information has been requested by the Financial Accountability Officer

- The information is not available through other sources

- The policy or financial decision to which the requested information relates has been made by the Executive Council and announced to the public or tabled with or disclosed to the Legislative Assembly, even if the Executive Council or one of its Committees will or could engage in future deliberations with respect to the decision

- The requested information is provided in a format that does not reveal other information protected by subsection 12(1) of the Freedom of Information and Protection of Privacy Act, including

- an agenda

- a Minute, unless the Minute is the only source of the requested information

- policy or costing options or recommendations prepared for or submitted to the Executive Council or its committees other than the policy or costing option selected for implementation

- the substance of the deliberations of the Executive Council or its committees regarding options or recommendations prepared for or submitted to the Executive Council or its committees, other than deliberations related to the policy option selected for implementation that would be apparent through the disclosure of the requested information

- information reflecting the individual opinions of members of the Executive Council

- a communications plan, stakeholder management plan, key messages, or other communications materials

- draft legislation or regulations other than the particular draft approved by the Executive Council

- The information would not reveal personal information or personal health information protected from disclosure by subsection 12(3) of the Financial Accountability Officer Act

- The Financial Accountability Officer agrees not to disclose the information without the consent of the Executive Council

- The provision of the information to the Financial Accountability Officer does not waive or limit the authority of the Head of an institution to apply the mandatory exemption of section 12(1) of the Freedom of Information and Protection of Privacy Act should the information be requested by any parties other than the Financial Accountability Officer.

Premier and President of the Council

Approved and Ordered: October 5, 2016

Footnotes

[1] Standing Order 108(e).

[2] Standing Orders 58, 61, 63.

[3] Standing Order 62. Special warrants and Treasury Board orders can allow expenditures without direct approval by the Assembly, though the latter must be offset by reducing other authorized expenditures: Financial Administration Act, RSO 1990, c F.12, ss 1.0.7-1.0.8. Both must be publicly reported under Standing Order 68.

[4] Constitution Act, 1867, ss 54, 90; Standing Order 57.

[5] In the current session, which began in September 2016, the Legislature has enacted three budget implementation acts: Building Ontario Up for Everyone Act (Budget Measures), 2016, SO 2016, c 37; Stronger, Healthier Ontario Act (Budget Measures), 2017, SO 2017, c 8; Budget Measures Act (Housing Price Stability and Ontario Seniors’ Public Transit Tax Credit), 2017, SO 2017, c 17.

[6] See e.g. Ontario Loan Act, 2017, SO 2017, c 8, Sched 26, s 1(1).

[7] See e.g. Supply Act, SO 2017, c 4.

[8] Standing Order 64.

[9] Standing Order 67(a).

[10] See e.g. Interim Appropriation Act for 2017-2018 Act, 2016, SO 2016, c 37, Sched 11.

[11] See e.g. Supplementary Interim Appropriation Act for 2016-2017, 2016, SO 2016, c 37, Sched 24.

[12] Standing Order 60.

[13] Standing Order 117(b).

[14] Standing Order 108(h).

[15] Standing Order 117(b).

[16] Standing Order 111(a).

[17] Paul Thomas & Graham White, “Evaluating Provincial and Territorial Legislatures” in Christopher Dunn, ed, Provinces: Evaluating Provincial and Territorial Politics, 3rd ed (Toronto: University of Toronto Press, 2016) 363 at 374–379; Tracey Raney, “The Ontario Legislature: Living Up to its Democratic Potential Amidst Political Change?” in Cheryl N Collier & Jonathan Malloy, eds, The Politics of Ontario (Toronto: University of Toronto Press, 2017) 81 at 94–95.

[18] SO 2015, c 31, Sched 1.

[19] RSO 1990, c F.31.

[20] The Executive Council consists of the Premier and ministers appointed by the Lieutenant Governor on advice of the Premier: Constitution Act, 1867, s 63; Executive Council Act, RSO 1990, c E.25, ss 1–2(1). The Executive Council is informally referred to as Cabinet.

[21] Ministry of Consumer & Commercial Relations (Re), Order P-226, 1991 CanLII 4020 (ON IPC).

[22] Ministry of Finance (Re), Order PO-2320, 2004 CanLII 56438 (ON IPC).

[23] See e.g. Standing Order 65; Fiscal Transparency and Accountability Act, 2004, SO 2004, c 27.

[24] OC 1412/2016 (https://www.ontario.ca/orders-in-council/oc-14122016).

[25] PC 1985-3783; PC 2006-1289; PC 2017-517.

[26] Official Report of Debates (Hansard), 37th Leg, 1st Sess, No 61 (18 May 2000) (Hon Gary Carr).

[27] Since Stephen LeClair was appointed effective March 2, 2015, the Board of Internal Economy approved a combined budget for March 1 to 31, 2015 and April 1, 2015 to March 31, 2016.

[28] The office incurred $312,300 (net of HST) in leasehold improvement costs for the renovation of its office space during the 13-month period ending on March 31, 2016. In accordance with the lease agreement, the landlord reimbursed the leasehold improvement costs in July 2016. As a result, the actual expense for services in 2015-16 was $386,554.