Assessing Ontario’s Medium-term Prospects

1. Executive Summary

FAO Projects a Return to Significant Budget Deficits

Despite a strong boost to revenues this year, the FAO is projecting an Ontario budget deficit of $4.0 billion in 2017-18, the result of the Auditor General of Ontario’s recommended accounting treatment for both the government’s Fair Hydro Plan and the net pension assets of jointly-sponsored pension plans.[1]

Beyond 2017-18, the FAO is projecting a significant increase in the budget deficit due to the loss of time-limited revenues, a more moderate pace of tax revenue growth, and the growing fiscal impact from the Fair Hydro Plan. By 2021-22, the FAO is projecting a budget deficit of $9.8 billion, in the absence of any fiscal policy changes. This is a significant deterioration since the FAO’s spring outlook[2] and is primarily the result of the introduction of the Fair Hydro Plan, which will add $3.2 billion to the budget deficit by 2021-22, under the Auditor General’s recommended accounting treatment.

In contrast, under the government’s accounting framework, the FAO projects a small budget surplus in 2017-18, and a return to budget deficits beginning in 2018-19 due to the loss of temporary revenues and moderate growth in tax revenues.

Since the government has not adopted the Auditor General’s recommended accounting for both the Fair Hydro Plan and net pension assets, it is becoming more difficult for legislators and the public to assess the government’s fiscal projections. This has reduced the transparency and reliability of Ontario’s fiscal plan.

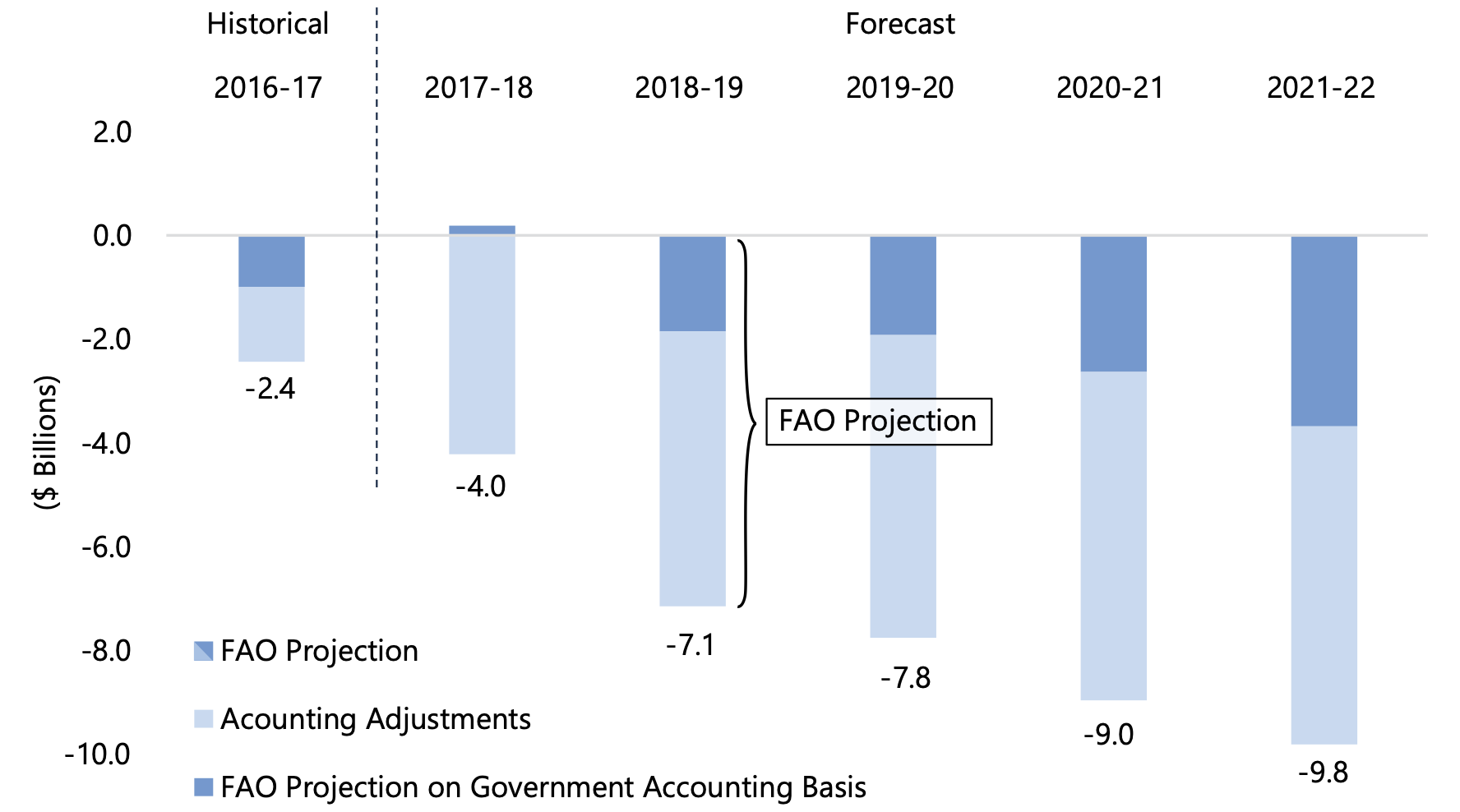

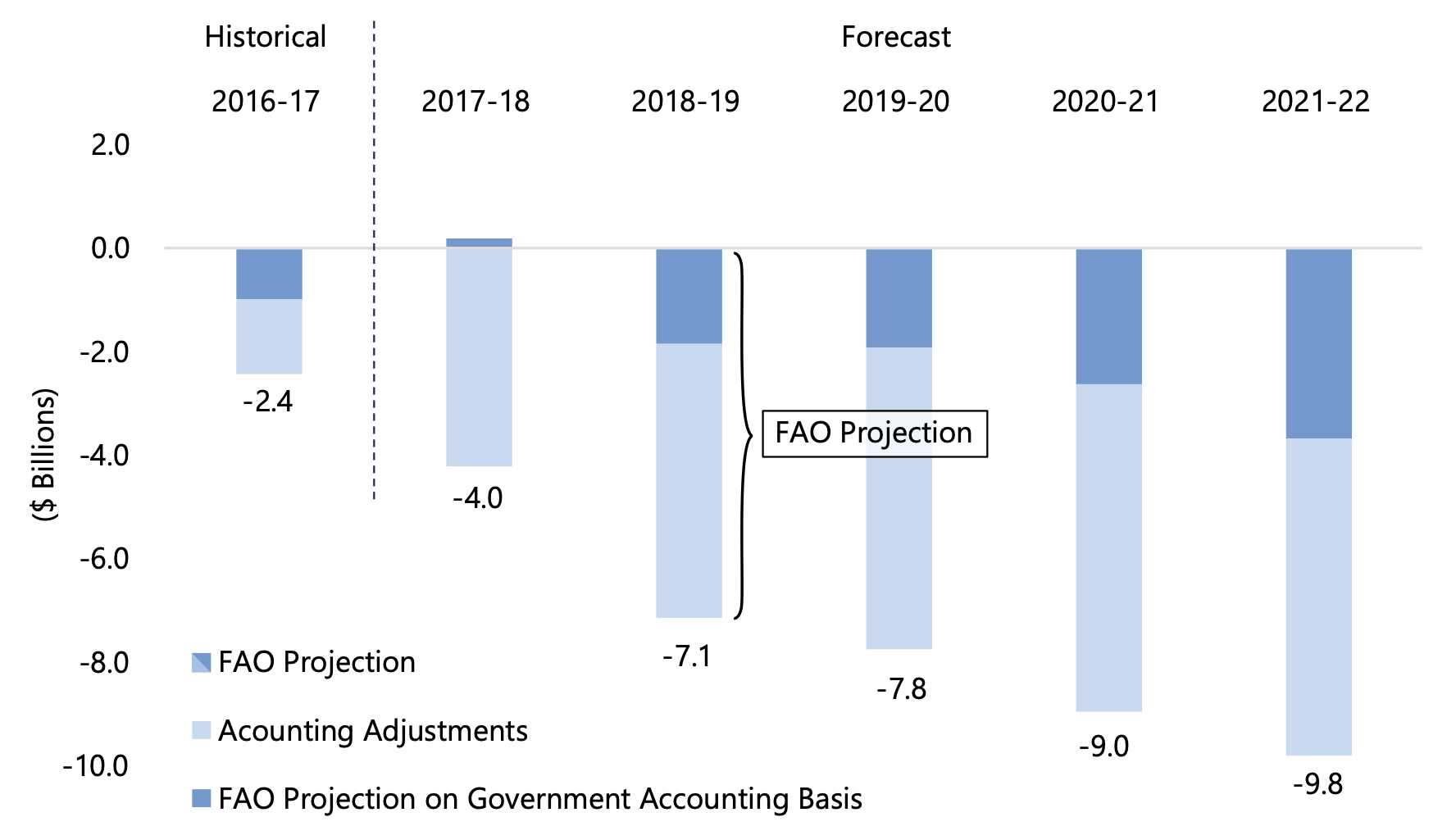

Ontario Budget Balance

Note: Budget Balance before reserve.

Source: Ontario Public Accounts, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart shows Ontario’s budget balance before the reserve from 2016-17 to 2021-22 under two different bases: the FAO’s forecast based on the government’s accounting presentation and the FAO’s forecast based on the Auditor General’s (AG) recommended accounting presentation.

The FAO’s forecast based on the AG’s recommended presentation shows a deficit of $4.0 billion in 2017-18, rising to a deficit of $9.8 billion by 2021-22.

In contrast, under the government presentation, the FAO projects a small surplus in 2017-18. However, the budget balance deteriorates to $3.7 billion by 2021-22.

The FAO is projecting very strong growth for the Ontario economy in 2017. Consistent with the outlook of most economic forecasters, the FAO expects the economy will grow at a more measured pace beginning in 2018. However, Ontario’s economic performance could worsen if the renegotiation of NAFTA impairs Ontario’s access to the US market, or if households reduce discretionary spending due to high debt levels and rising interest rates.

Total revenues are forecast to increase by 3.5 per cent per year on average over the outlook, somewhat slower than the rate of GDP growth. This reflects the loss of time-limited revenues in 2018-19, as well as moderating tax revenue growth over the outlook. By comparison, the FAO projects program spending will grow by 4.4 per cent on average from 2017-18 to 2021-22, when all spending related to the Fair Hydro Plan is included.

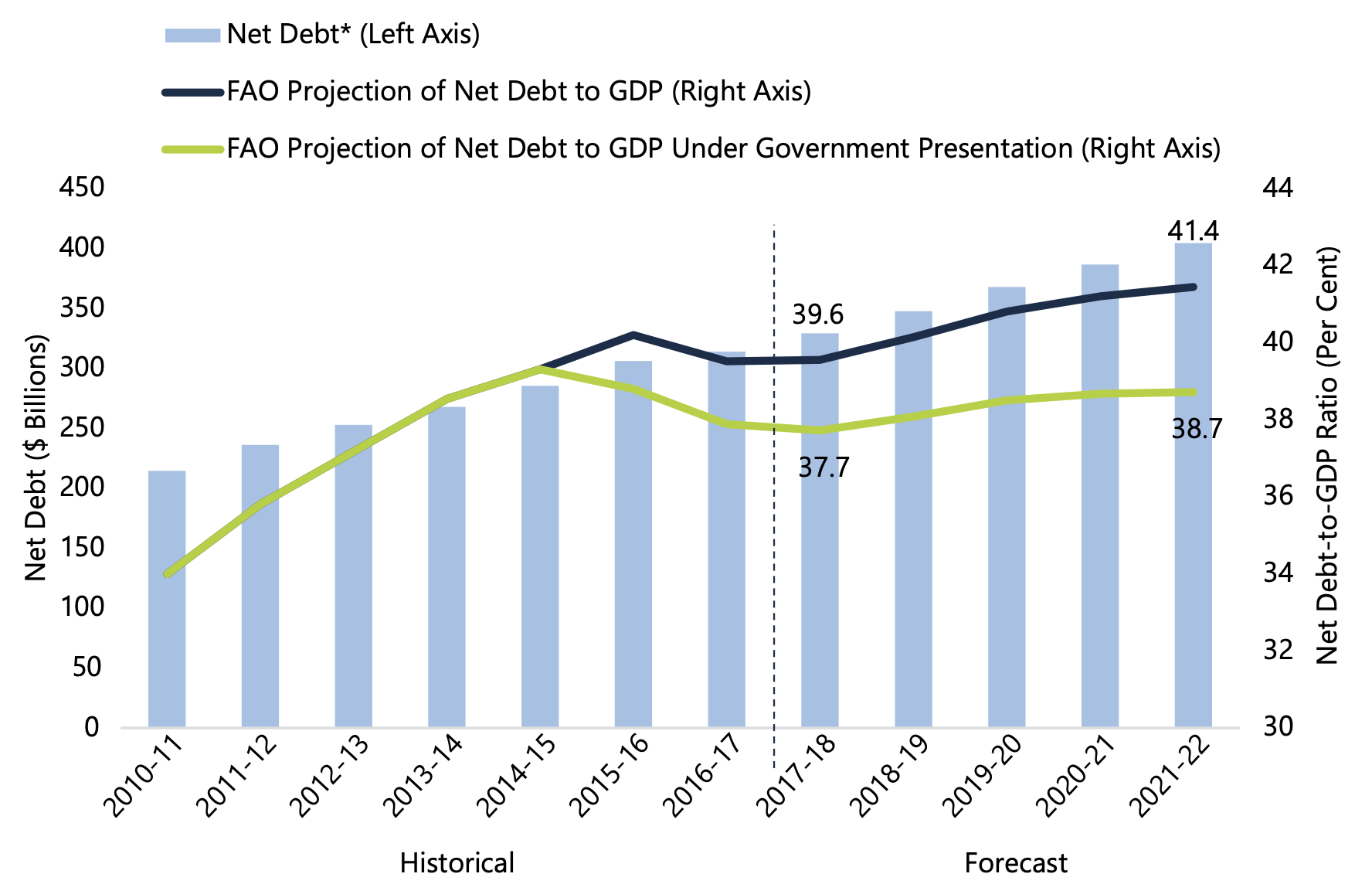

The FAO projects Ontario’s net debt-to-GDP ratio will remain essentially unchanged in 2017-18 at just under 40 per cent. However, over the next four years, the FAO expects that without any change to current fiscal policies, approximately $75 billion will be added to Ontario’s net debt, increasing the net debt-to-GDP ratio to over 41 per cent by 2021-22.[3] In contrast, the government continues to maintain a net debt-to-GDP target of 35 per cent by 2023-24 and 27 per cent by 2029-30.

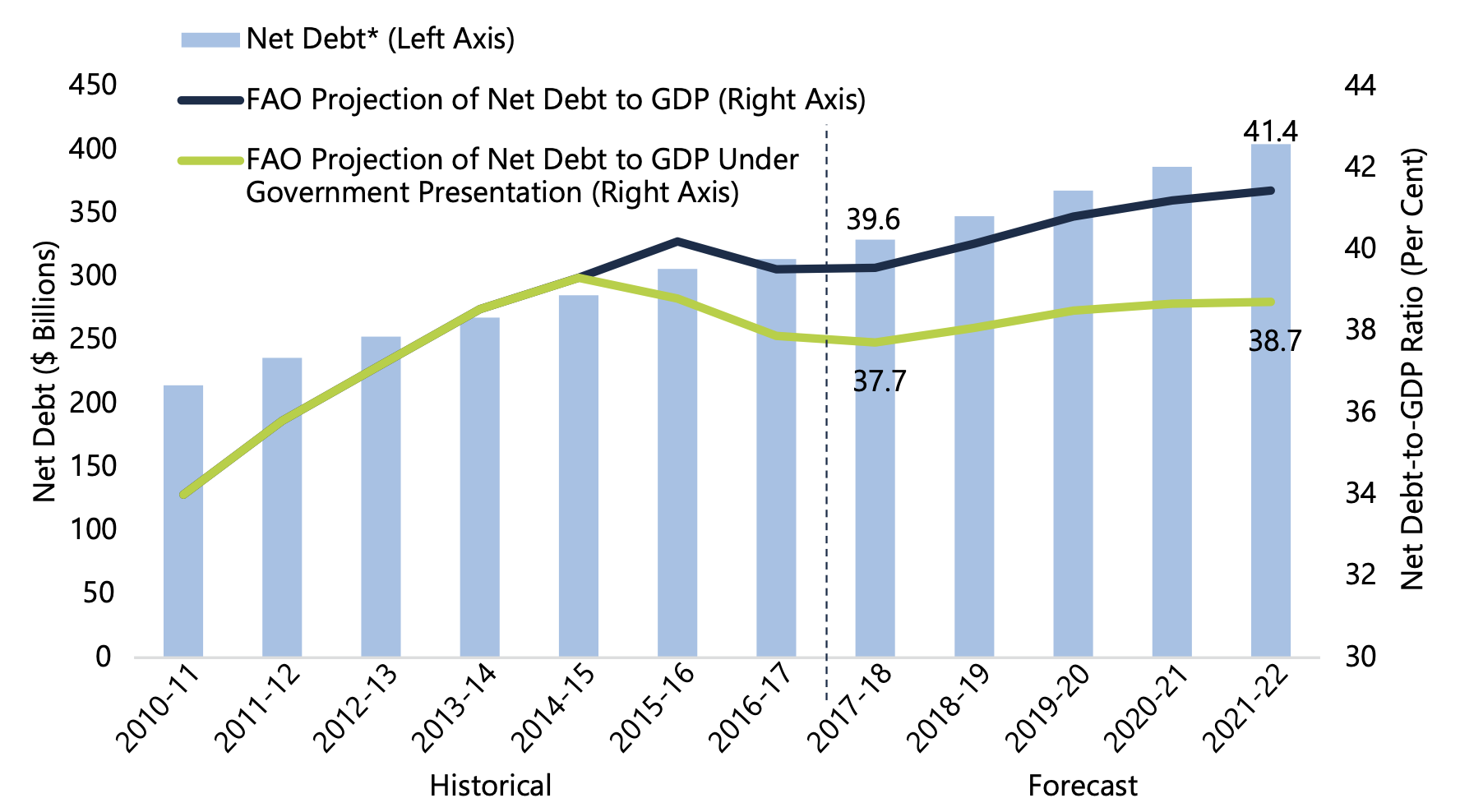

Net Debt Outlook

* Net debt is presented on the AG’s recommended accounting basis, which includes the impact of the Fair Hydro Plan and the pension adjustment.

Source: 2017 Ontario Economic Outlook and Fiscal Review, Ontario Public Accounts and FAO.

Accessible version

This chart shows the historical and forecasted net debt-to-GDP ratio from 2010-11 to 2021-22 under two different bases: the FAO’s forecast based on the AG’s recommended presentation and the FAO’s forecast based on the government’s presentation. The FAO’s forecast based on the AG’s accounting presentation shows net debt-to-GDP rising over the outlook from 39.6 per cent in 2017-18 to 41.4 per cent by 2021-22, whereas the FAO’s forecast based on the government’s accounting presentation shows net debt-to-GDP rising from 37.7 per cent in 2017-18 to 38.7 per cent by 2021-22. The chart also shows total net debt, based on the AG’s accounting presentation, which rises to over $400 billion by 2021-22.

Current and future Ontario governments are facing difficult policy choices. Based on the FAO’s fiscal projection, additional measures to raise revenue or lower spending will be required if the Province intends to achieve and maintain a balanced budget, and lower Ontario’s debt burden.

2. Economic Outlook

Overview

Ontario Economy Exceeding Expectations in 2017

Following a strong performance over the first half of 2017, the Ontario economy is expected to continue on a path of solid growth into 2018.

Led by a continued surge in household spending and residential investment, the FAO projects Ontario real GDP growth of 2.8 per cent in 2017, an upward revision from the FAO’s spring outlook report. Nominal GDP – the broadest measure of the tax base – is projected to increase by 4.7 per cent in 2017, well above the FAO’s spring forecast. The strong growth in nominal GDP in 2017 is supported by significant gains in corporate profits.

Beginning in 2018, most forecasters, including the FAO, expect the Ontario economy to grow at a more measured pace, as growth in the US and Canadian economies is also expected to moderate. At the same time, higher interest rates are expected to contribute to slower growth of household spending and residential investment over the outlook.

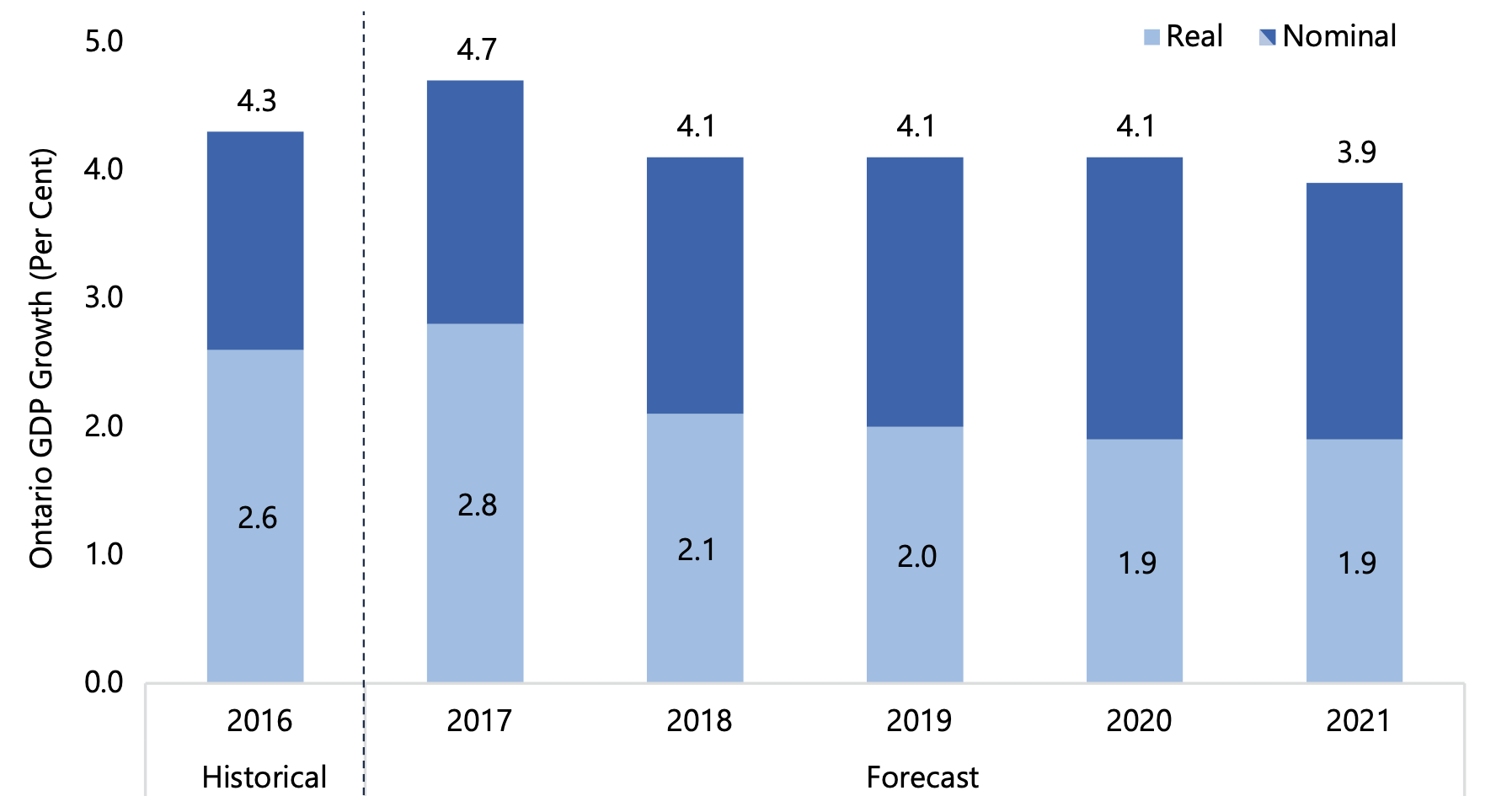

Solid Economic Performance Expected Over Outlook

Source: Ontario Economic Accounts, Statistics Canada and FAO.

Accessible version

This chart shows the FAO’s forecast for nominal and real GDP from 2016 to 2021. Real GDP grew by 2.6 per cent in 2016. The FAO forecasts real GDP growth of 2.8 per cent in 2017, moderating to 2.1 per cent in 2018, 2.0 per cent in 2019 and 1.9 per cent in 2020 and 2021. Nominal GDP grew by 4.3 per cent in 2016. The FAO forecasts nominal GDP growth of 4.7 per cent in 2017, 4.1 per cent from 2018 to 2020 and 3.9 per cent in 2021.

Global Economic Growth Gaining Traction

In its latest World Economic Outlook, the International Monetary Fund (IMF) revised up its forecast for global economic growth to 3.6 per cent in 2017 and 3.7 per cent in 2018.[4] A number of key economies reported stronger than expected growth over the first half of 2017, including the euro area and Japan. These upward revisions more than offset weaker than expected growth in the United Kingdom and the United States.

United States

In the US, real GDP is expected to grow by 2.2 per cent in 2017. Following a modest first-quarter gain, US consumer spending has shown signs of strengthening while business investment remains strong, particularly in the energy sector. Going forward, the FAO projects US growth to ease slightly to 1.9 per cent by 2021.

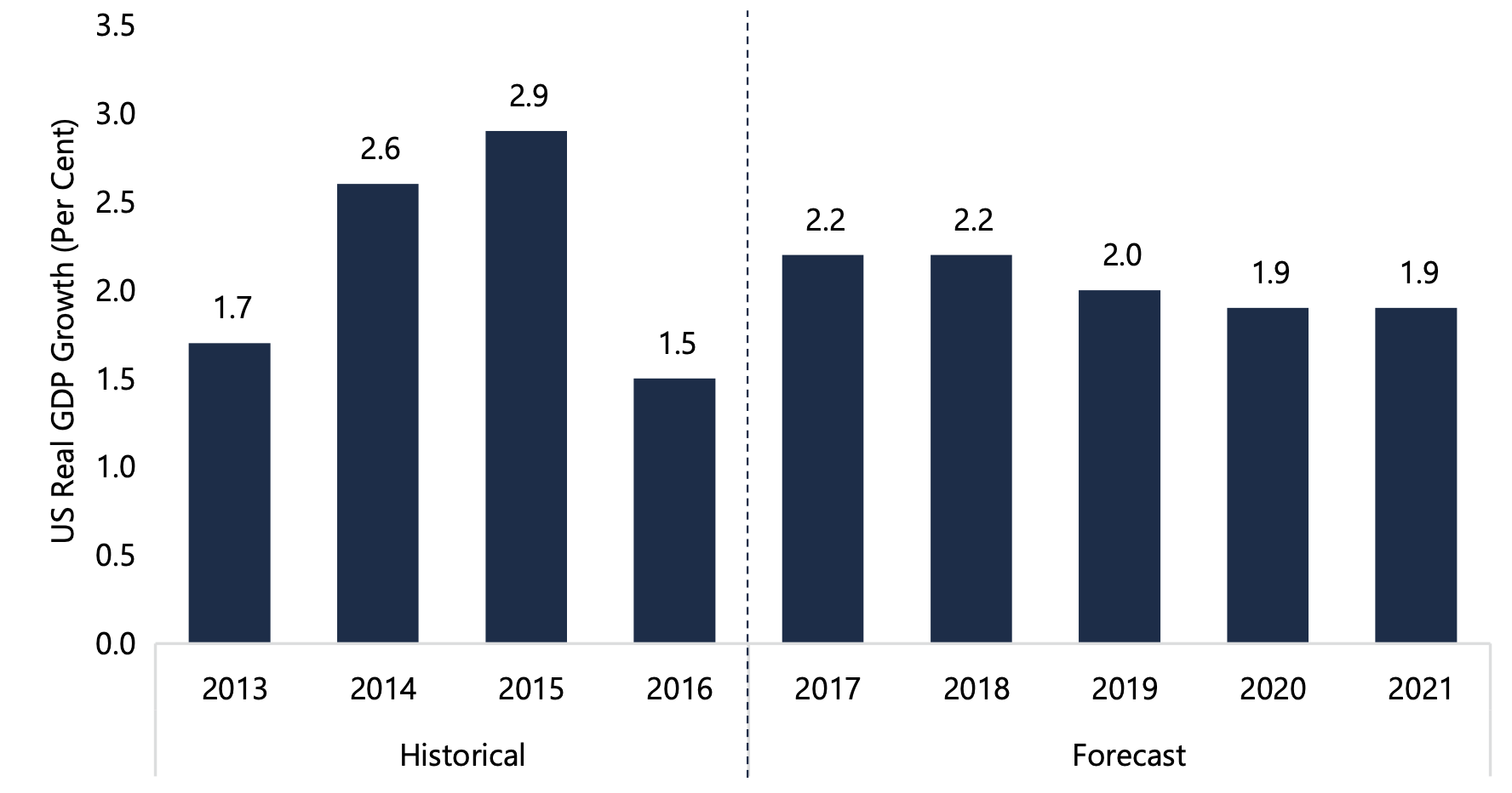

US Economic Growth to Moderate

Source: US Bureau of Economic Analysis, Congressional Budget Office and FAO Consensus.

Accessible version

This chart shows the historical and forecasted U.S. real GDP growth rates from 2013 to 2021. The U.S. economy grew by 1.7 per cent in 2013, 2.6 per cent in 2014, 2.9 per cent in 2015 and by 1.5 per cent in 2016. U.S. growth is expected to reach 2.2 per cent in 2017 and 2018 and average 1.9 per cent from 2019 to 2021.

However, the outlook for the US economy depends critically on the uncertain policy direction of the current US administration. Significant tax reform, including sizable tax cuts, have been proposed, although it is unclear if an agreement in Congress will be reached. Likewise, the renegotiation of the North American Free Trade Agreement (NAFTA) is ongoing, and the potential impact of a new trade agreement on North American economies remains highly uncertain (see ‘Key Risks’ for more details).

Other World Economies

The IMF reports that the euro area economy continues to gain strength, supported by a pick-up in exports and continued strength in domestic demand. In China, the IMF expects economic growth to ease from 6.8 per cent in 2017 to 6.5 per cent in 2018. While the Chinese economy is continuing to rebalance towards more consumption-led growth, debt continues to build among households, government and businesses, which could pose risks to medium-term growth.[5]

While the global economy is expected to perform solidly through 2018, over the medium term, global growth is expected to be limited by modest productivity gains, aging workforces in advanced economies, and tightening financial conditions.

Canadian Economy

The Canadian economy is on track to post the strongest annual growth since 2011. Robust consumer spending, and a pickup in exports and business investment supported solid overall Canadian growth during the first half of 2017. While consumer spending and exports are expected to moderate over the second half of the year, the Canadian economy is on pace for a 3.1 per cent annual gain in 2017. The FAO expects Canadian real GDP to grow by 2.1 per cent in 2018 and by an average of 2.0 per cent through 2021, as higher interest rates contribute to slower growth in consumer spending and residential investment.

The brisk pace of economic growth over the first half of the year led the Bank of Canada to increase its policy interest rate to 0.75 per cent in July and 1.0 per cent in September. Importantly, the Bank indicated that with the Canadian economy operating near full capacity, it will take a cautious, data-driven approach in determining future rate increases. Given the Bank’s measured approach and the subdued rate of consumer price inflation, the FAO expects a gradual but steady rise in interest rates over the medium-term, consistent with the FAO’s spring outlook.

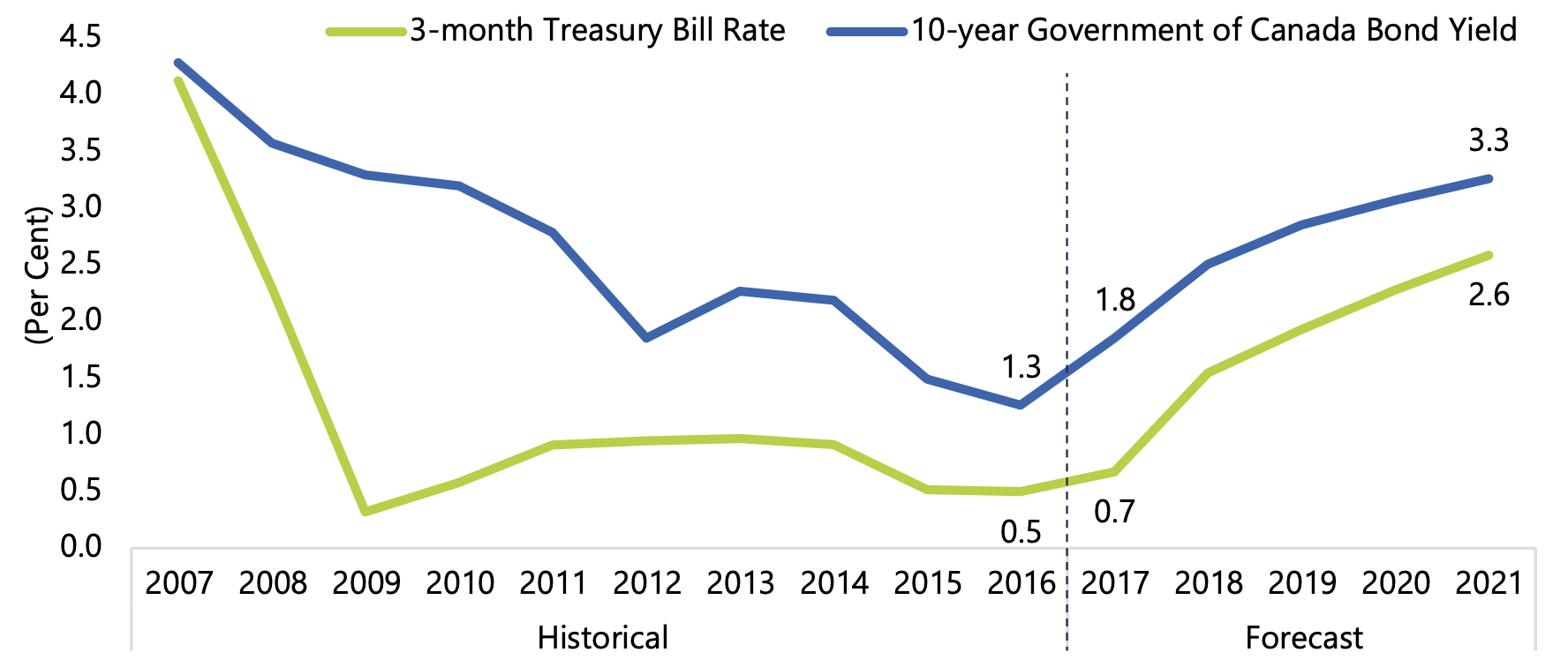

The recent increases in Canadian interest rates contributed to an eight-cent appreciation in the Canadian dollar relative to the US dollar through the summer, before reversing some of this gain more recently. With this appreciation, the FAO projects that the dollar will average 78 cents in 2017, slightly higher than the FAO’s spring outlook. Going forward, the FAO expects a gradual appreciation of the dollar to about 81 cents by 2021, supported by a steady rise in Canadian interest rates and a moderate increase in oil prices.

Canadian Interest Rates to Rise over the Outlook

Source: Statistics Canada and FAO.

Accessible version

This chart shows the historical and forecasted 3-month Treasury bill rate and the 10-year Government of Canada bond yield from 2007 to 2021. The 3-month Treasury bill rate declined from 4.1 per cent in 2007 to 0.5 per cent in 2016, and is expected to rise modestly to 0.7 per cent by 2017 and continue to rise, reaching 2.6 per cent by 2021. The 10-year Government of Canada bond yield declined from 4.3 per cent in 2007 to 1.3 per cent in 2016, and is expected to rise to 1.8 per cent by 2017 and continue to rise, reaching 3.3 per cent by 2021.

Ontario Economic Outlook

Solid 2017 Growth Expected to Moderate over the Outlook

Ontario posted solid real GDP growth of 2.6 per cent in 2016, the third consecutive year of strong growth for the economy. The FAO expects that the economy’s momentum will continue into 2017, with real GDP advancing by 2.8 per cent.

Household Spending Primary Driver of Growth in 2017

* Business Investment includes both Non-Residential Investment and Machinery & Equipment Investment.

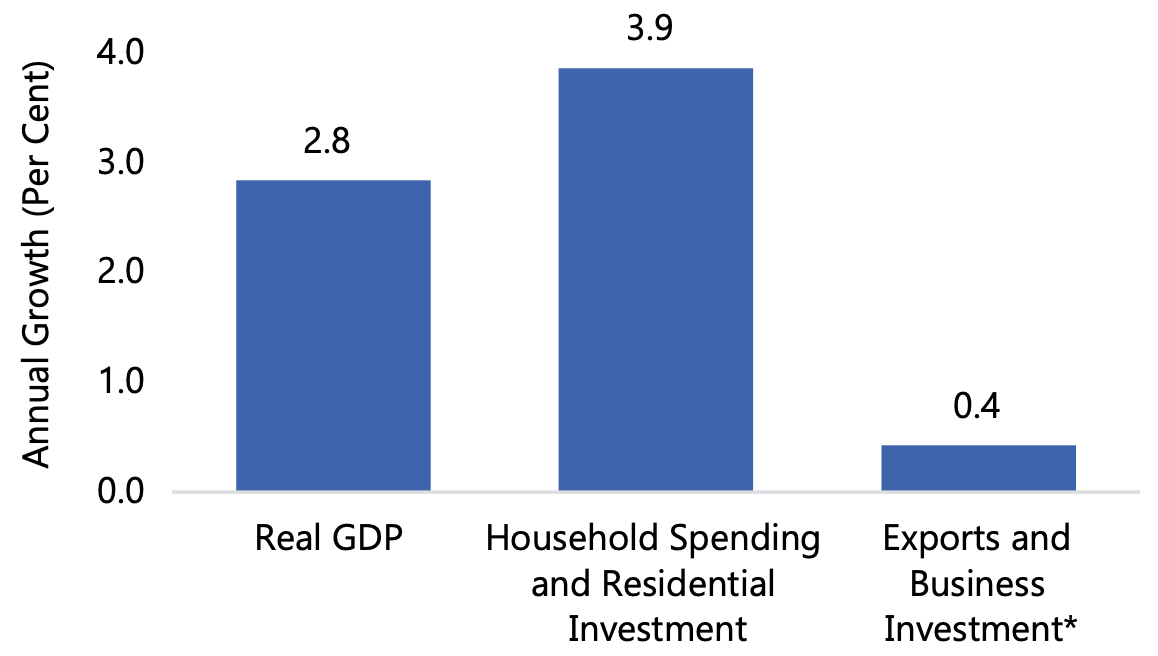

Source: Statistics Canada, Ontario Economic Accounts and FAO.

Accessible version

This chart shows the 2017 growth rates for three categories: (1) Ontario real GDP, (2) household spending and residential investment and (3) exports and business investment. Real GDP is expected to grow at an annual rate of 2.8 per cent in 2017. Growth in household spending and residential investment is expected to be 3.9 per cent. Growth in exports and business investment is expected to be 0.4 per cent.

However, despite the projection for relatively strong economic growth in 2017, the drivers of that growth are unbalanced. Household spending and residential construction are providing the main support for the economy’s growth in 2017, while exports and business investment have underperformed.

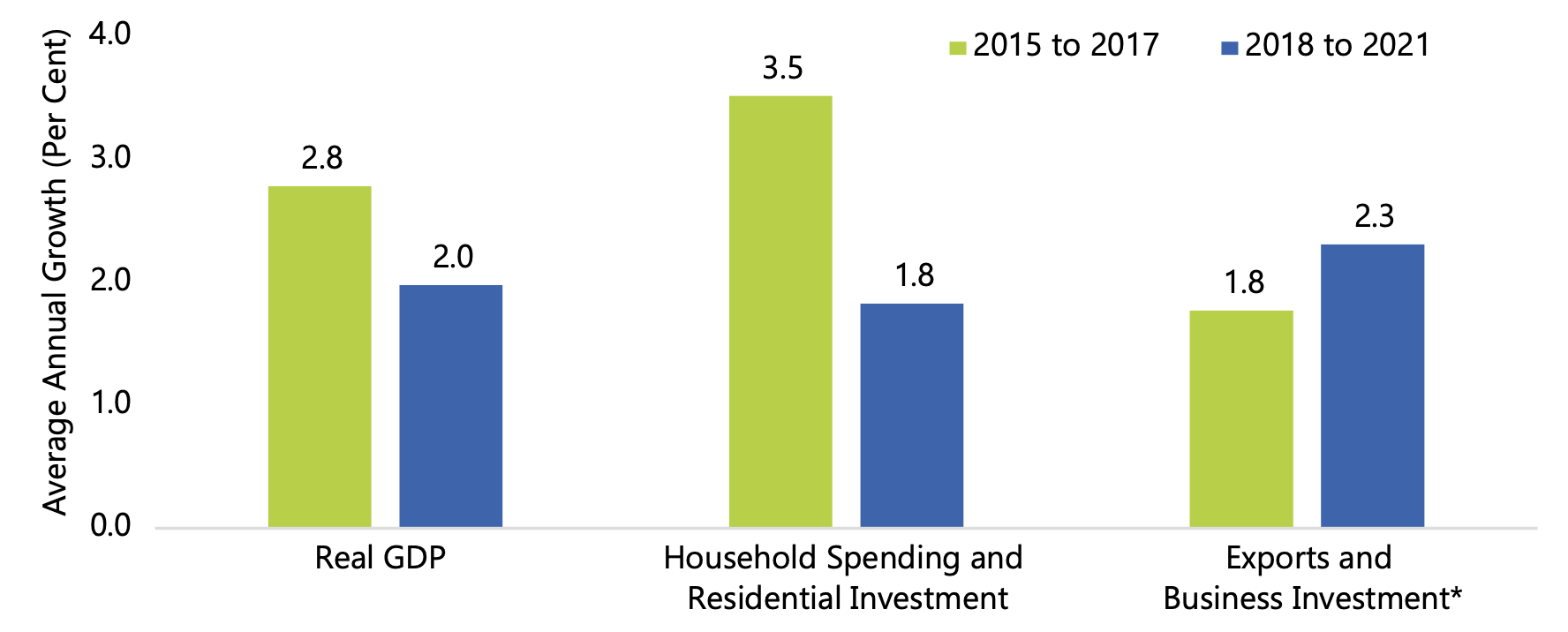

Going forward, the FAO expects that elevated levels of household debt combined with rising interest rates will hamper household spending and residential investment. At the same time, exports and business investment are expected to contribute more to economic growth, as sustained foreign demand encourages businesses to increase production capacity (discussed further in ‘Key Risks’ below). Over the outlook, the FAO projects real GDP growth will ease to 2.1 per cent in 2018 and average 1.9 per cent per year from 2019 to 2021.

Exports and Business Investment Expected to Drive Growth over the Outlook

* Business Investment includes both Non-Residential Investment and Machinery & Equipment Investment.

Source: Statistics Canada, Ontario Economic Accounts and FAO.

Accessible version

This chart shows average growth rates over the periods 2015 to 2017 and 2018 to 2021 for three categories: (1) Ontario real GDP, (2) household spending and residential investment and (3) exports and business investment. Real GDP growth is expected to slow from 2.8 per cent over 2015 to 2017 to 2.0 per cent over 2018 to 2021. Growth in household spending and residential investment is expected to drop from an average of 3.5 percent over 2015 to 2017 to 1.8 per cent over 2018 to 2021. Growth in exports and business investment is expected to increase from 1.8 per cent over 2015 to 2017 to 2.3 per cent over 2018 to 2021.

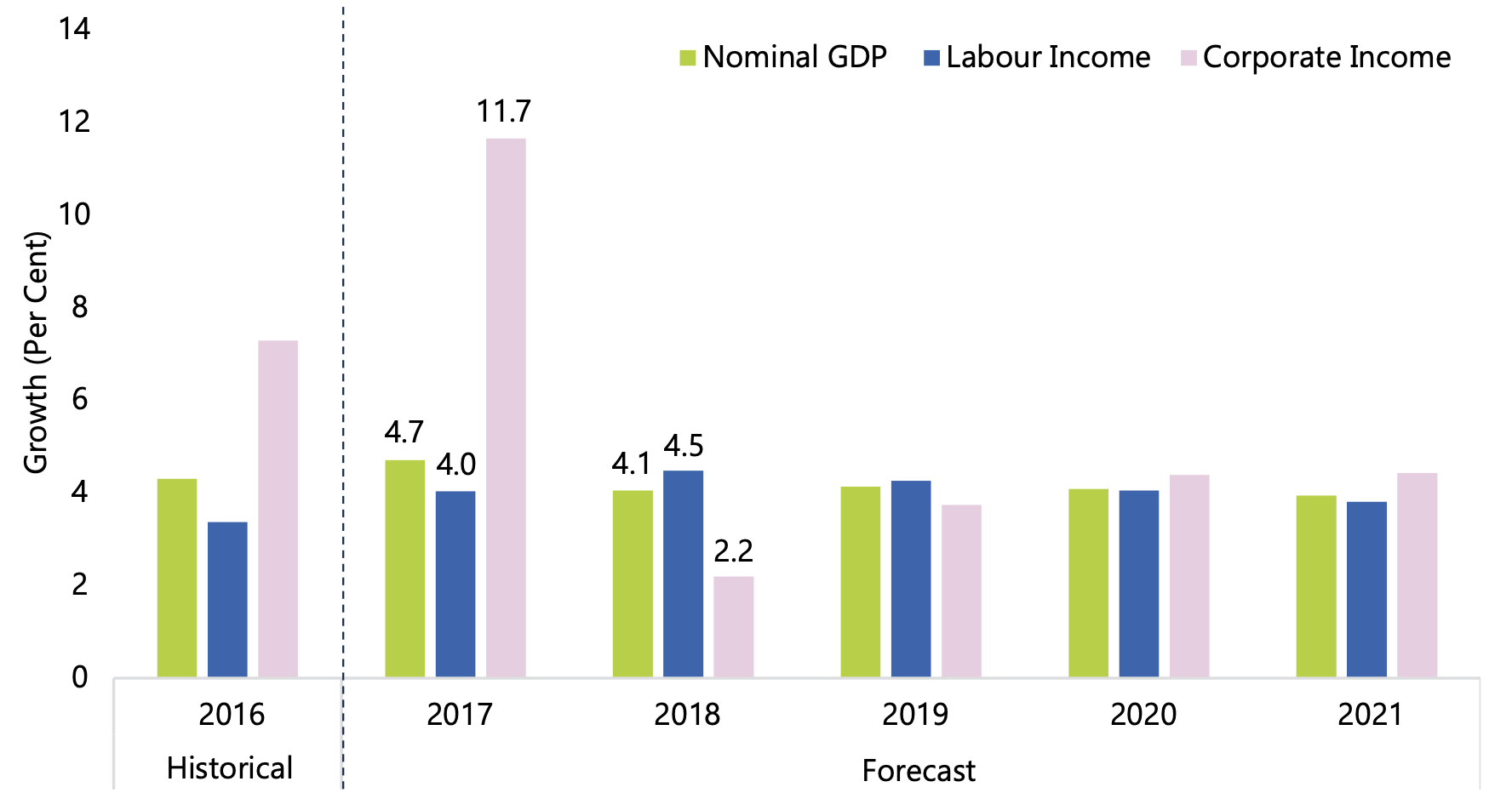

Strong Gain in Corporate Profits Projected for 2017

The FAO is forecasting nominal GDP growth of 4.7 per cent in 2017, driven by an 11.7 per cent increase in corporate profits, and a more moderate gain of 4.0 per cent in labour income.

The planned increases to Ontario’s minimum wage are expected to raise labour income growth in 2018 and 2019.[6] Beyond 2019, labour income growth is expected to moderate to 3.8 per cent by 2021.

Slower labour income gains will contribute to slightly more moderate nominal GDP growth of 3.9 per cent by 2021.

Corporate Income Leads Nominal GDP Growth in 2017

Note: Labour and corporate income comprise roughly 70 per cent of nominal GDP. The other categories include mixed income (from proprietorships) and net taxes.

Source: Statistics Canada, Ontario Economic Accounts and FAO.

Accessible version

This chart shows historical and forecasted annual growth rates from 2016 to 2021, for nominal GDP and two of its main subcomponents, labour income and corporate income. The graph illustrates that nominal GDP is expected to grow at a slightly higher rate in 2017 than in 2016, primarily driven by very strong growth in corporate income. In 2018 corporate income is expected to fall, accompanied by a slight decrease in nominal GDP and slight gain in labour income. The three categories are all expected to grow at roughly 4 per cent from 2019 to 2021.

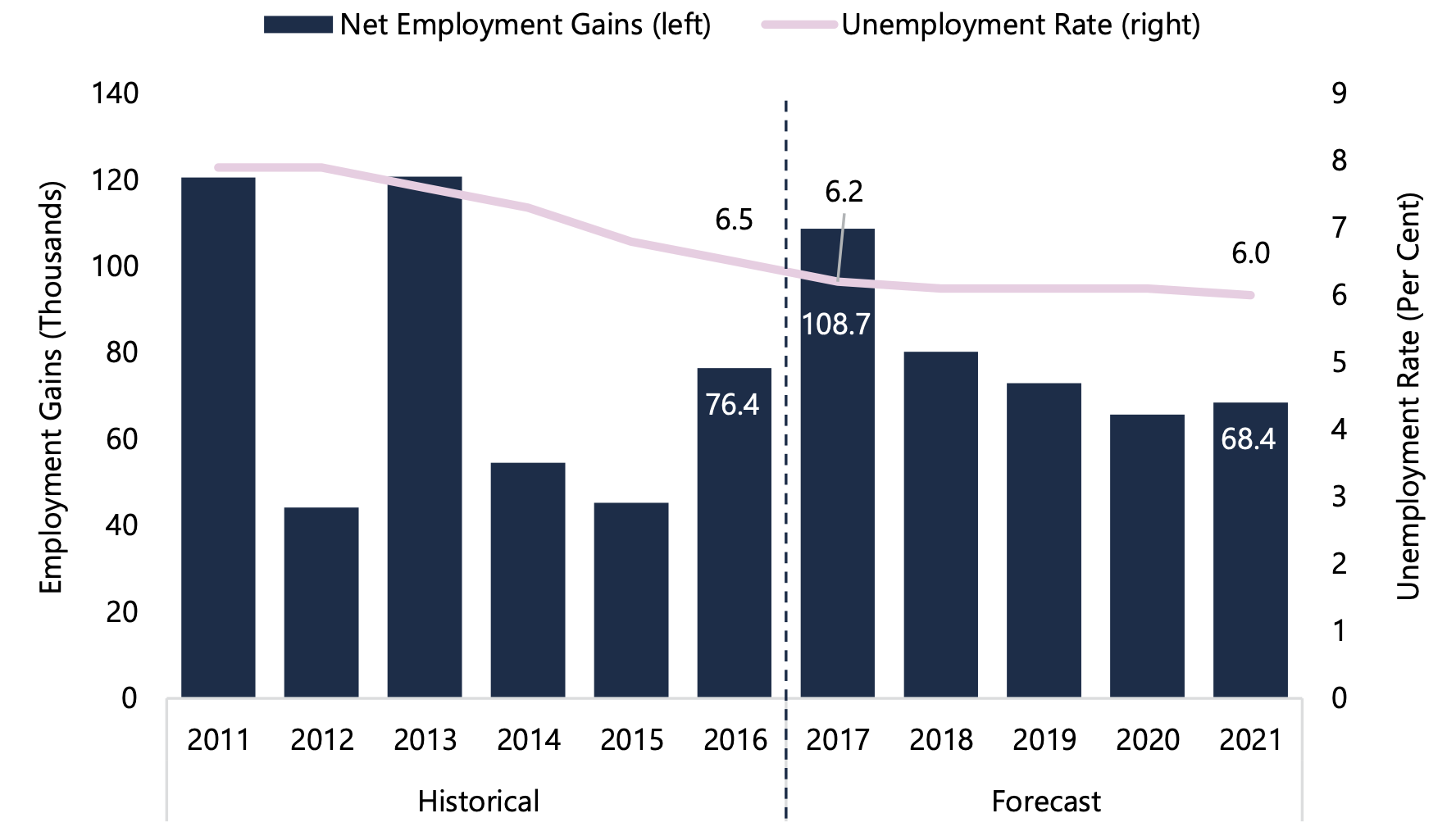

Steady Job Gains Expected to Continue

The FAO is projecting strong job growth of 1.6 per cent (+109 thousand net new jobs) in 2017, following a gain of 1.1 per cent (+76 thousand net new jobs) in 2016.

Over the outlook, sustained economic growth is expected to support average annual employment growth of 1.1 per cent, just slightly faster than the growth in the labour force. As a result, the unemployment rate is expected to trend lower, falling from 6.2 per cent in 2017 to 6.0 per cent by 2021.

Steady Employment Gains as Unemployment Rate Trends Lower

Source: Statistics Canada and FAO.

Accessible version

This chart shows historical and forecasted net employment gains and unemployment rate from 2011 to 2021. The chart shows that the unemployment rate has been declining since 2011 and is expected to continue to decline, falling from 6.5 per cent in 2016 to 6.2 per cent in 2017 and continuing to decline, reaching 6.0 per cent by 2021. Net employment gains are expected to be 108,700 in 2017 compared to 76,400 in 2016. Net employment gains are expected to continue over the outlook, but at successively smaller levels, with job growth of 68,400 by 2021.

Key Risks for Ontario’s Economic Outlook

While the FAO expects solid economic growth over the medium-term, there are a number of risks that could negatively affect Ontario’s economic performance.

Most economic forecasters, including the FAO, continue to assume that NAFTA will largely be maintained in its current form. However, the US administration is demanding significant concessions from Canada and Mexico, and has threatened to leave NAFTA altogether. Some businesses may already be postponing investment decisions outside of the United States due to the uncertainty surrounding NAFTA. If the renegotiation of NAFTA leads to a deterioration in Ontario’s terms of trade or restricts access to the US market, there would be significant negative implications for the province’s growth prospects.

In recent years, strong growth in household spending has not been matched by similar gains in household incomes, leading to higher levels of household debt. In 2016, household debt reached 167 per cent of disposable income in Ontario, a significant rise from 149 per cent in 2010.[7] Higher debt burdens expose households to financial risk. With a steady rise in interest rates expected over the next few years, many households will scale back discretionary spending in order to make higher debt interest payments, which in turn could have implications for the pace of overall economic growth.[8]

There are also upside risks that could lead to a stronger economic performance for Ontario. In particular, some forecasters expect the US economy will grow faster over the medium-term than the FAO projects.[9] Stronger than projected US growth would lift demand for Ontario’s exports, raising employment and leading to stronger wage and profit growth for the province.

3. Fiscal Outlook

FAO Projects a Return to Significant Budget Deficits

Despite a strong increase in revenues, the FAO is projecting an Ontario budget deficit of $4.0 billion in 2017-18, entirely the result of the Auditor General of Ontario’s recommended accounting treatment for both the government’s Fair Hydro Plan (FHP)[10] and the net pension assets of jointly-sponsored pension plans.[11]

Beyond 2017-18, the FAO is projecting substantial increases in the budget deficit due to the loss of time-limited revenues, a more moderate pace of tax revenue growth, and the growing fiscal impact of the FHP and the pension adjustment. By 2021-22, the FAO is projecting an Ontario budget deficit of $9.8 billion in the absence of any fiscal policy changes.

This is a significant deterioration since the FAO’s spring outlook, primarily due to the government’s introduction of the FHP,[12] which will add $3.2 billion to the budget deficit by 2021-22.

Ontario Budget Balance

Note: Budget Balance before reserve.

Source: Ontario Public Accounts, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart shows Ontario’s budget balance before the reserve from 2016-17 to 2021-22 under two different bases: the FAO’s forecast based on the government’s accounting presentation and the FAO’s forecast based on the Auditor General’s (AG) recommended accounting presentation.

The FAO’s forecast based on the AG’s recommended presentation shows a deficit of $4.0 billion in 2017-18, rising to a deficit of $9.8 billion by 2021-22.

In contrast, under the government presentation, the FAO projects a small surplus in 2017-18. However, the budget balance deteriorates to $3.7 billion by 2021-22.

In the 2017 Ontario Economic Outlook and Fiscal Review (also referred to as the Fall Economic Statement or FES), the government projected balanced budgets for 2017-18 through to 2019-20. However, the government’s fiscal projection relies on an overly optimistic revenue forecast and does not adopt the Auditor General’s recommended accounting for FHP or net pension assets.[13]

For comparison, under the government’s accounting presentation, the FAO projects a small budget surplus for 2017-18, approximately equal to the government’s projection in the Fall Economic Statement. However, there are a number of time-limited and one-time revenues which contribute to the budget balance in 2017-18. Going forward, the loss of these temporary revenues combined with more moderate tax revenue growth results in a return to deficit in 2018-19 and a steady deterioration in the budget deficit over the outlook.

The Accounting Presentation of Ontario’s Financial Statements

In both the 2017 Ontario Budget and Fall Economic Statement, the government has not adopted the Auditor General’s recommended accounting framework, reducing the transparency and reliability of Ontario’s fiscal projections.

In addition to the existing disagreement over the appropriate accounting treatment for the government’s jointly sponsored pension plans, the Auditor General recently reported that the government is not correctly accounting for the full cost of the Fair Hydro Plan in its fiscal plan. As a result, the government’s financial statements are expected to continue to receive qualified opinions from the Auditor General.

Revenue Outlook

The FAO is projecting average annual revenue growth of 3.5 per cent over the forecast. In 2017-18, revenues are supported by strong growth in taxes, as well as a number of time-limited or one-time revenues. Beginning in 2018-19, the FAO is projecting more moderate revenue growth as:

- time-limited revenues end (including asset sales and federal Equalization payments); and

- economic growth moderates, following several years of stronger than average growth.

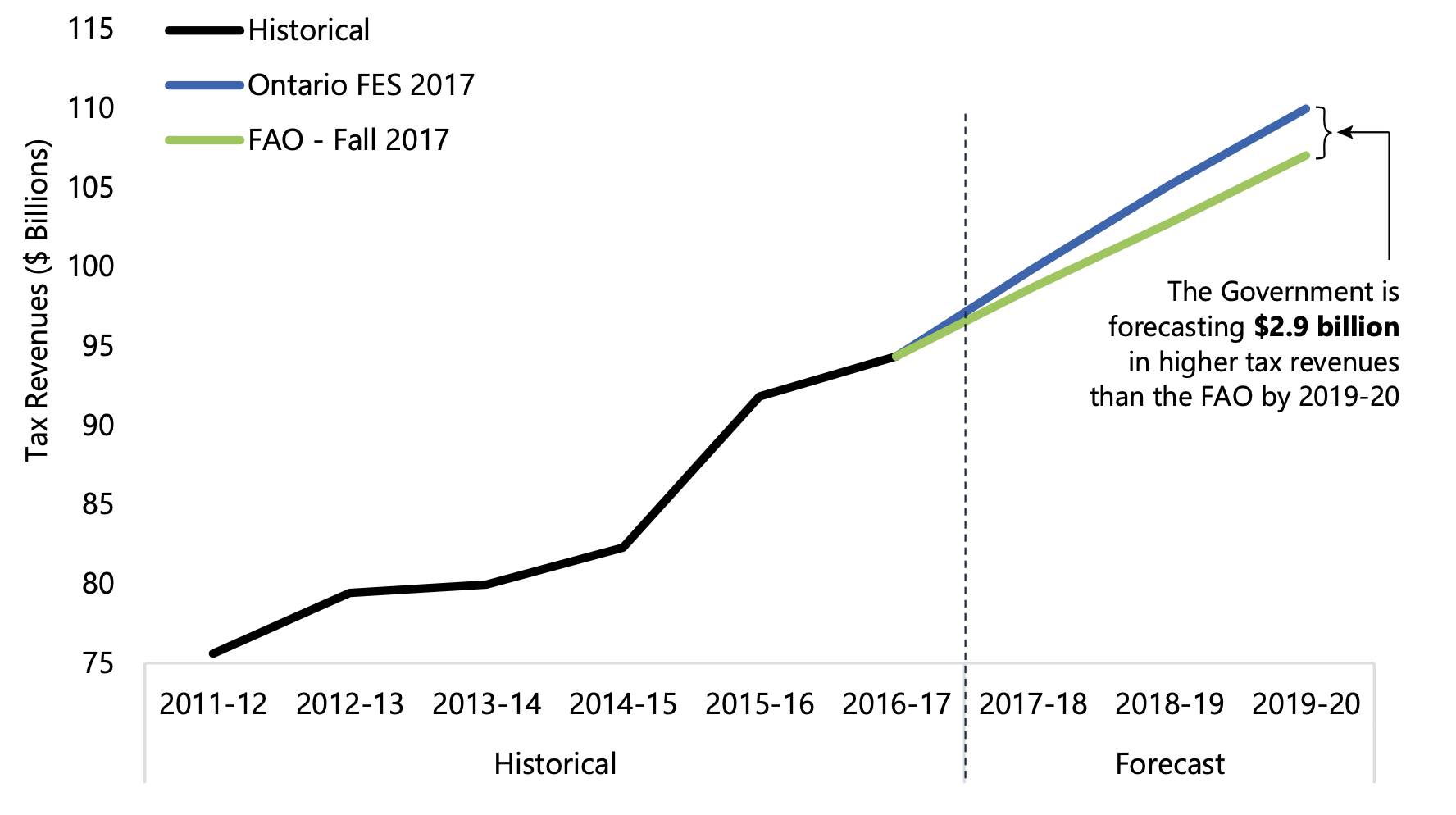

Tax Revenue Growth Expected to Moderate

Nominal GDP, the broadest measure of the tax base, is projected to grow by a strong 4.7 per cent in 2017, supporting a 4.6 per cent increase in tax revenues in 2017-18. From 2018 to 2021, annual GDP growth is expected to moderate to 4.1 per cent, leading to similar slowing in tax revenue growth to 4.1 per cent on average over this period.

In the government’s Fall Economic Statement, tax revenue is projected to grow by 5.2 per cent on average from 2017-18 to 2019-20, much higher than the FAO’s projection of 4.3 per cent over the same period. The government’s expectation of higher growth results in an additional $2.9 billion in tax revenues by 2019-20, relative to the FAO projection.

FAO’s Taxation Revenue Outlook

Source: Ontario Public Accounts, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

The chart shows historical and forecasted total tax revenue from 2011-12 to 2019-20, comparing the FAO’s Fall 2017 Outlook to the government’s 2017 Ontario Economic and Fiscal Review. The chart illustrates that the FAO is projecting slightly lower tax revenue compared to the 2017 Ontario Economic and Fiscal Review. The difference grows steadily, reaching a value of $2.9 billion by 2019-20.

The government’s revenue forecast relies on optimistic projections for many of the key economic drivers of tax revenue, including labour income, corporate income, and household spending. In particular, the government is forecasting:

- significant and sustained above-trend growth in labour income;

- a surge in 2017 corporate income growth; and

- continued strength in household spending, despite higher interest rates and elevated levels of household debt.

Taken together, the government’s revenue forecast appears to be based on overly optimistic projections for the three main revenue drivers.[14]

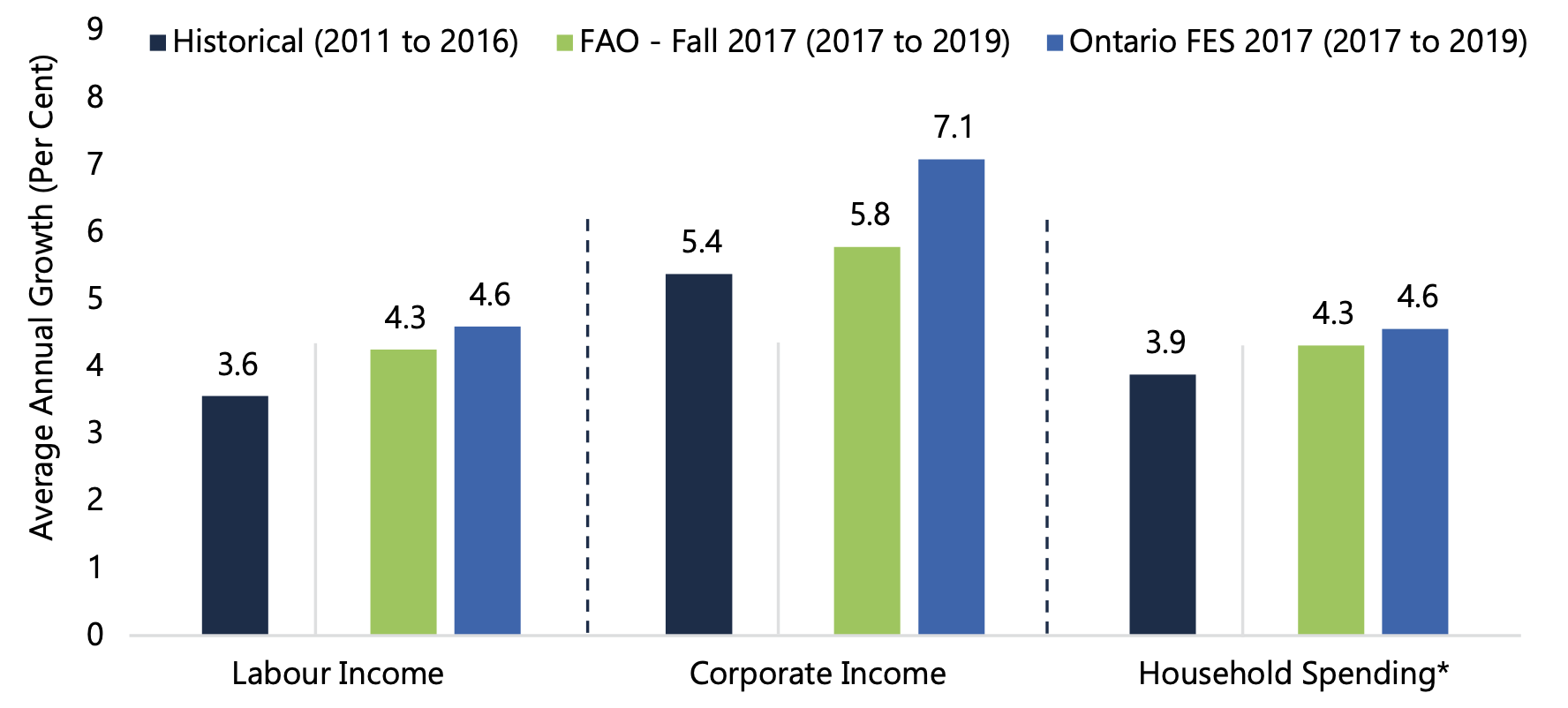

Growth in Key Tax Drivers

* The FES forecast for Household Spending is calculated as Real Household Spending plus CPI inflation.

Source: Statistics Canada, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart compares the historical and forecasted growth rates for labour income, corporate income and household spending. Labour income is forecasted to grow by 4.3 per cent on average annually from 2017 to 2019 by the FAO and 4.6 per cent over the same period in the FES, a significant increase from the 3.6 per cent growth from 2011 to 2016. Corporate income grew by 5.4 per cent from 2011 to 2016, and is forecast to grow by 5.8 per cent by the FAO and 7.1 per cent by the FES between 2017 and 2019. Household spending grew by 3.9 per cent from 2011 to 2016, and is forecast to grow by 4.3 per cent by the FAO and 4.6 per cent by the FES between 2017 and 2019.

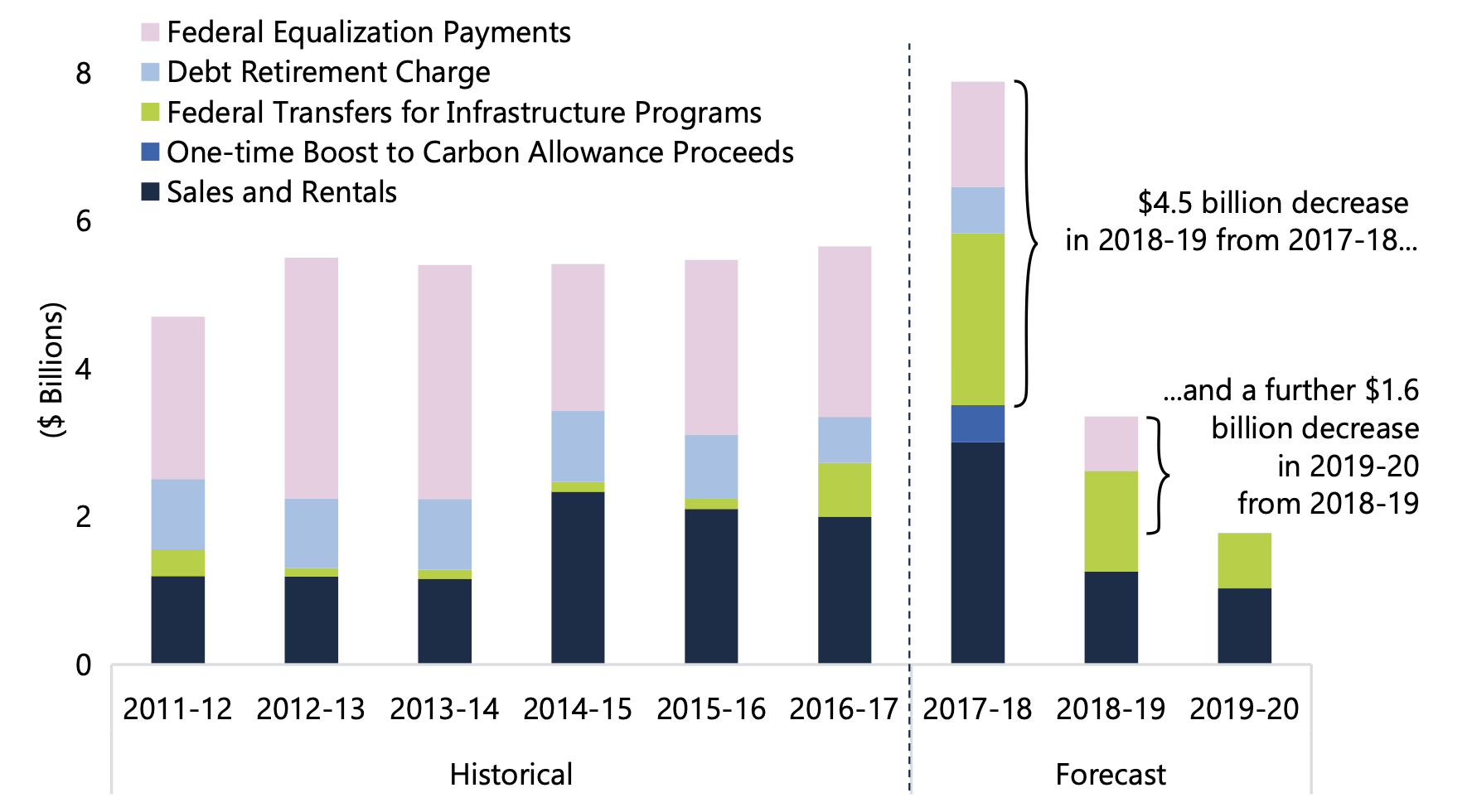

The Loss of Time-limited Revenues

The revenue projection for 2017-18 includes a number of one-time or time-limited revenues that are set to expire.[15] These include:

- a temporary increase to sales and rentals revenue, reflecting additional asset sales[16];

- higher federal transfers for infrastructure;

- the final year of the debt retirement charge[17];

- federal Equalization payments, which the FAO estimates will end in 2019-20; and

- additional, one-time proceeds from Ontario’s cap and trade program in 2017-18.[18]

Taken together, these time-limited revenues will decrease by $4.5 billion in 2018-19, and by an additional $1.6 billion in 2019-20.

Many Time-limited Revenues are Set to Expire Beyond 2017-18

Source: Ontario Budgets, Ministry of Finance and FAO.

Accessible version

The chart shows revenues from federal Equalization payments, the Debt Retirement Charge, federal transfers for infrastructure programs, one-time cap-and-trade proceeds, and sales and rentals from 2011-12 to 2019-20. The chart shows that these revenue sources are going to strengthen by $2.2 billion in 2017-18 before falling by $4.5 billion in 2018-19 and a further $1.6 billion in 2019-20.

| Revenue Source | Assumption | Forecast |

|---|---|---|

| Taxation Revenue | Grows with key economic drivers including labour income, corporate income and household spending | Averages 4.2 per cent growth per year from 2017-18 to 2021-22* |

| Federal Transfers | Based on legislated growth rates and economic forecasts for Ontario and Canada | Federal transfers are expected to grow by 1.6 per cent per year from 2017-18 to 2021-22 |

| Government Business Enterprises (GBE) | Based on government projections. | Income from GBEs are projected to rise moderately from $5.6 billion in 2016-17 to $6.7 billion in 2021-22 |

| Other Revenue | Based on government projections, and includes asset sales, and proceeds from the sale of cap and trade allowances | These revenues are projected to increase from $16.3 billion in 2016-17 to $19.4 billion in 2017-18, before declining to $18.0 billion by 2021-22 |

Expense Outlook

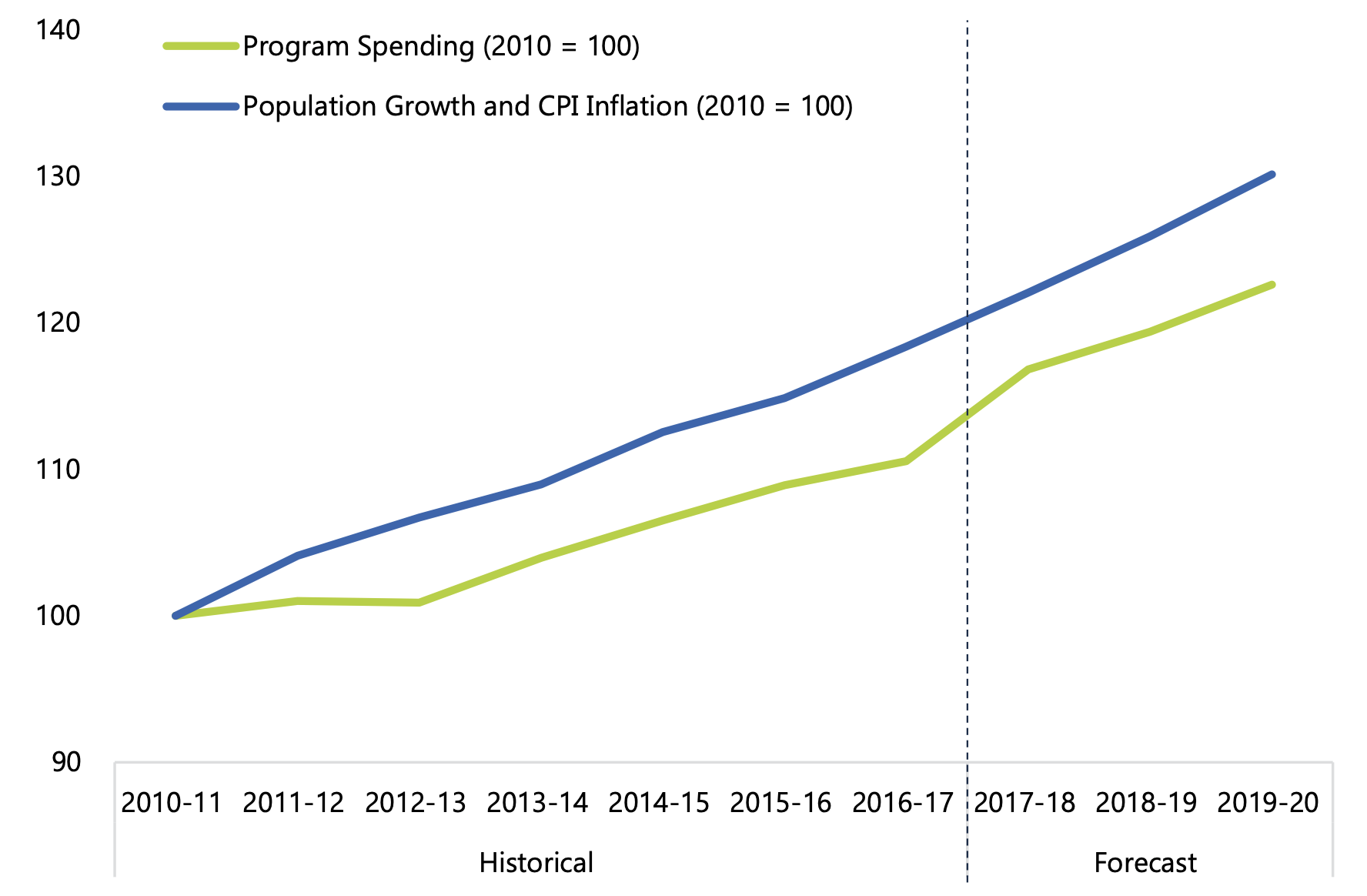

Program Spending

In the 2010 Budget, the government introduced a plan to return to balanced budgets by 2017-18. Since then, the government has restrained the average growth of program spending to below the rate of inflation and population growth.

Program Spending and Spending Pressures

Source: Ontario Public Accounts, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart compares historical and forecasted program spending with spending pressures (population growth and inflation) from 2010-11 to 2019-20. Both series are indexed to their 2010-11 values. The chart shows that the government has restrained spending growth below the rate of inflation and population growth and is planning to continue doing so over their forecast horizon (2017-18 to 2019-20).

Over the 2017-18 to 2019-20 period, the FAO’s outlook adopts the government’s 2017 Fall Economic Statement projections for program spending but makes adjustments to reflect the Auditor General’s recommended accounting presentation.[19] Excluding these adjustments, the projection for program spending is largely unchanged from the 2017 Ontario Budget, aside from $200 million of new spending beginning in 2017-18.[20]

In 2017-18, program spending is expected to grow by 5.7 per cent.[21] This spending includes additional funding for health care, education and elements of the Fair Hydro Plan. However, in 2018-19 and 2019-20, the government plans to restrain increases in program spending to an average of 2.4 per cent, below the growth in underlying spending pressures.

Beyond 2019-20, the FAO projects that program spending will grow by an annual average rate of 4.2 per cent. This stronger pace of growth reflects additional spending to meet underlying pressures. In particular, the aging baby boomer cohort and the growing youth population will place added spending pressures on Ontario’s health care and education systems in the near future.

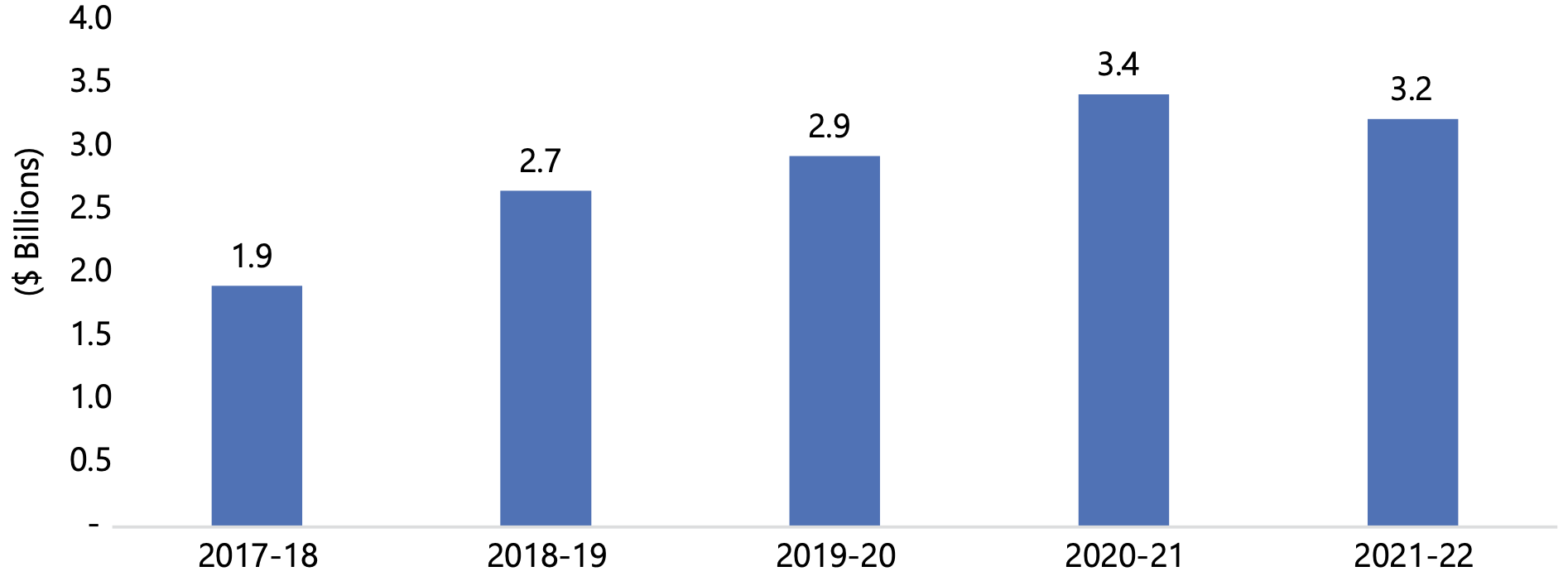

Impact of the Fair Hydro Plan

The government introduced the “Fair Hydro Plan” to reduce electricity bills for residential customers by an average of 25 per cent. The FHP includes refinancing a portion of the reduced electricity costs for ratepayers through borrowing by the Province and Ontario Power Generation (OPG).

The Auditor General has recommended that the cost of this refinancing be fully captured as an expense. However, the government has not included this cost in its fiscal plan.

Consistent with the Auditor General’s recommendation, the FAO has included the full fiscal impact of the FHP in its projection by increasing program spending by an average of $2.8 billion per year over the outlook (See the FAO’s An Assessment of the Fiscal Impact of the Province’s Fair Hydro Plan for further details).

Impact of the Fair Hydro Plan on Ontario’s Program Spending

Source: FAO.

Accessible version

This chart shows the impact on program spending from the Fair Hydro Plan from 2017-18 to 2021-22. The cost is expected to be $1.9 billion in 2017-18, $2.7 billion in 2018-19, $2.9 billion in 2019-20, $3.4 billion in 2020-21 and $3.2 billion in 2021-22.

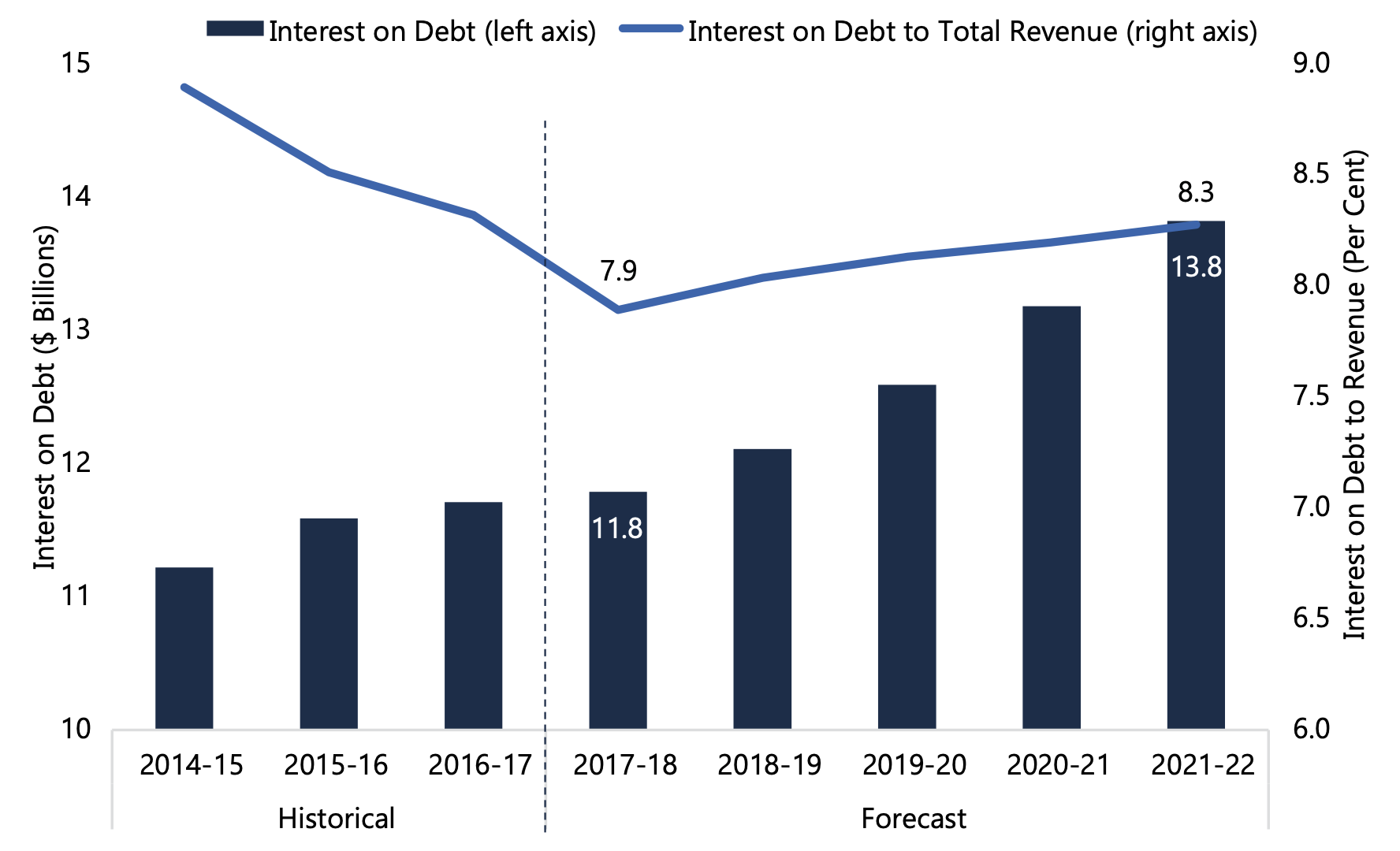

Interest on Debt

Interest on debt (IOD) payments are expected to increase at an average rate of 3.4 per cent per year over the outlook due to elevated borrowing levels and rising interest rates.

Over the past three years, IOD as a share of revenues has declined, a reflection of strong revenue growth, lower new borrowing and maturing debt being refinanced at much lower rates of interest. However, this trend is expected to reverse over the outlook as revenue growth moderates while IOD payments accelerate. By 2021-22, Ontario’s debt interest payments will account for 8.3 per cent of total revenue, above the 7.9 per cent share in 2017-18.

Interest on Debt

Source: Ontario Public Accounts, 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart shows the historical and forecasted level of interest on debt, and interest on debt as a share of revenue from 2014-15 to 2021-22. The graph illustrates that interest on debt is expected to rise from $11.7 billion in 2016-17 to $13.8 billion by 2021-22 and interest on debt as a share of revenues is expected to fall from 8.3 per cent in 2016-17 to 7.9 per cent in 2017-18 before steadily increasing to 8.3 per cent by 2021-22.

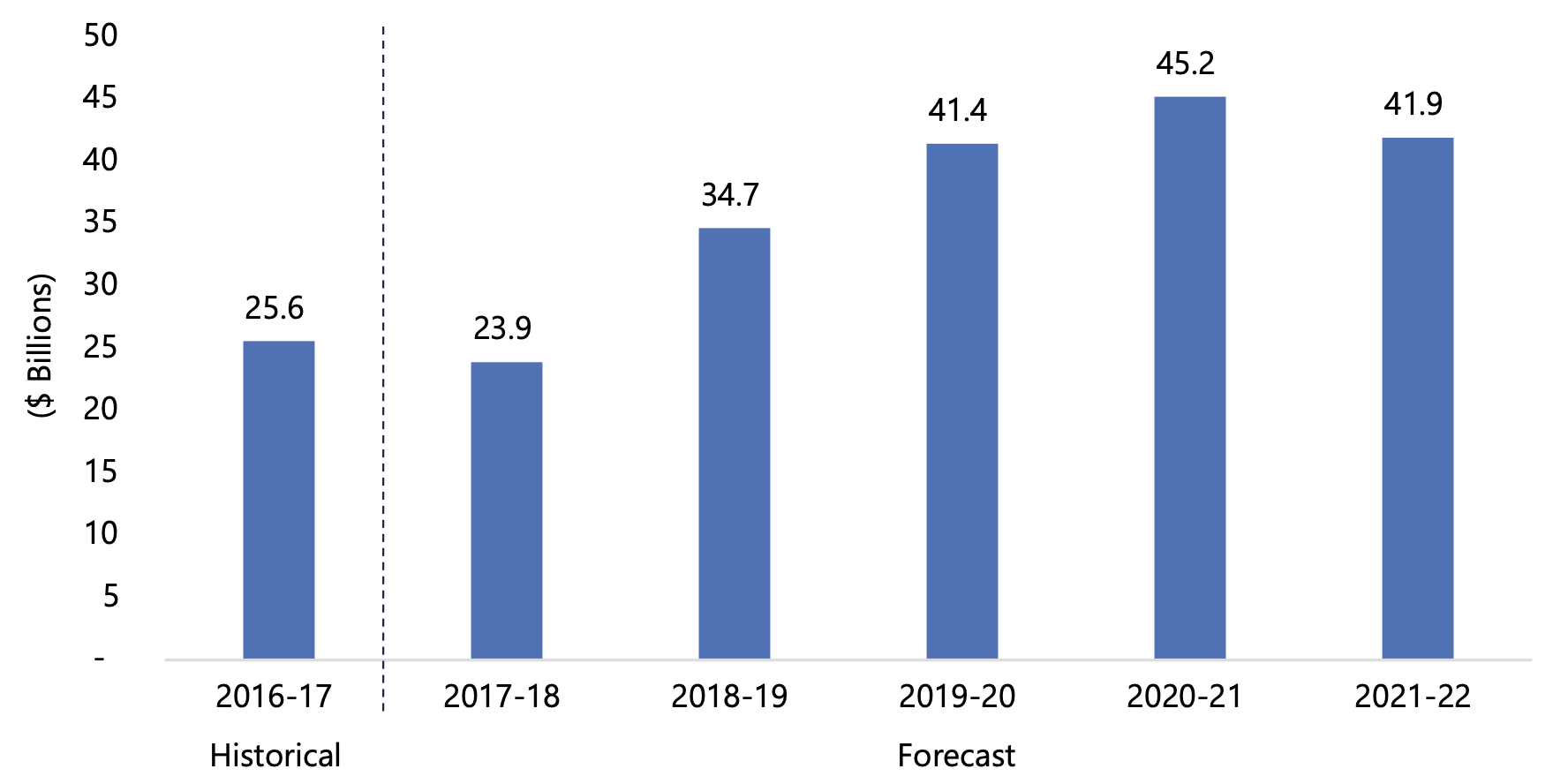

Borrowing and Net Debt

Despite higher funding requirements for capital expenditures and the Fair Hydro Plan, Ontario’s borrowing is expected to decline to $23.9 billion in 2017-18, the lowest level of borrowing since 2007.

However, beginning 2018-19, borrowing requirements are expected to increase significantly due to higher annual debt maturities, additional funding requirements for the Fair Hydro Plan and rising capital expenditures. By 2020-21, the FAO projects borrowing to increase to over $45 billion – nearly double the borrowing requirement in 2017-18.

Borrowing Outlook

Source: 2017 Ontario Economic Outlook and Fiscal Review and FAO.

Accessible version

This chart shows the historical and forecasted borrowing outlook from 2016-17 to 2021-22. Borrowing is expected to fall slightly from $25.6 billion in 2016-17 to $23.9 billion in 2017-18, before increasing to $34.7 billion in 2018-19, $41.4 billion in 2019-20, $45.2 billion in 2020-21 and $41.9 billion in 2021-22.

The FAO projects Ontario’s net debt-to-GDP ratio will remain essentially unchanged in 2017-18 at 39.6 per cent. However, over the next four years, the FAO projects that Ontario’s net debt will increase by approximately $75 billion to over $400 billion, increasing the net debt-to-GDP ratio to 41.4 per cent by 2021-22.[22]

Net Debt Outlook

Note: Net debt is presented on the Auditor General’s basis, which includes the fiscal impact of the Fair Hydro Plan and pension adjustment.

Source: 2017 Ontario Economic Outlook and Fiscal Review, Ontario Public Accounts and FAO.

Accessible version

This chart shows the historical and forecasted net debt-to-GDP ratio from 2010-11 to 2021-22 under two different bases: the FAO’s forecast based on the AG’s recommended presentation and the FAO’s forecast based on the government’s presentation. The FAO’s forecast based on the AG’s accounting presentation shows net debt-to-GDP rising over the outlook from 39.6 per cent in 2017-18 to 41.4 per cent by 2021-22, whereas the FAO’s forecast based on the government’s accounting presentation shows net debt-to-GDP rising from 37.7 per cent in 2017-18 to 38.7 per cent by 2021-22. The chart also shows total net debt, based on the AG’s accounting presentation, which rises to over $400 billion by 2021-22.

The government continues to maintain a net debt-to-GDP target of 35 per cent by 2023-24 and 27 per cent by 2029-30. However, the FAO’s net debt-to-GDP projections under both accounting presentations suggest that additional fiscal measures would be required for the government to achieve its net debt-to-GDP targets.

4. Appendix

Developments since the FAO’s Spring 2017 Economic and Fiscal Outlook

The FAO’s current projection of Ontario’s budget balance has deteriorated compared to the spring outlook.

- The Fair Hydro Plan, which boosts expenses by an average of $2.8 billion over the outlook, accounts for the majority of the higher deficit.

- In addition, compared to the spring, the FAO forecasts more moderate growth in revenues from personal income tax and the Land Transfer Tax over the outlook. This is offset by stronger expected growth in federal transfers and GBE income.

| 2016-17 | 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | |

|---|---|---|---|---|---|---|

| FAO’s 2017 Spring Budget Balance Forecast |

-5.0 | -2.9 | -4.9 | -5.5 | -6.0 | -6.5 |

| Developments Since Spring 2017 | ||||||

| Revenue | ||||||

| Taxation Revenue | 0.4 | -0.0 | -0.4 | -0.3 | -0.2 | -0.0 |

| Federal Transfers and GBE | -0.0 | 0.3 | 0.7 | 0.7 | 0.7 | 0.7 |

| Other Revenue Developments | 0.4 | 0.4 | 0.0 | -0.0 | -0.1 | 0.1 |

| Total | 0.8 | 0.7 | 0.3 | 0.4 | 0.5 | 0.9 |

| Expense | ||||||

| Fair Hydro Plan | – | 1.9 | 2.7 | 2.9 | 3.4 | 3.2 |

| Net New Spending* | -0.8 | 0.2 | 0.1 | -0.0 | 0.4 | 1.7 |

| Revised Adjustment for Pension Asset | -0.8 | -0.0 | -0.0 | -0.0 | -0.0 | -0.0 |

| Lower IOD Forecast | -0.2 | -0.2 | -0.2 | -0.3 | -0.5 | -0.7 |

| Total | -1.8 | 1.9 | 2.6 | 2.6 | 3.4 | 4.2 |

| Total Developments | 2.6 | -1.2 | -2.3 | -2.2 | -2.9 | -3.3 |

| FAO’s 2017 Fall Budget Balance Forecast |

-2.4 | -4.0 | -7.1 | -7.8 | -9.0 | -9.8 |

Forecast Tables

| (Per Cent Growth) | 2015a | 2016a | 2017f | 2018f | 2019f | 2020f | 2021f | Average* |

|---|---|---|---|---|---|---|---|---|

| Nominal GDP | ||||||||

| FAO – Fall 2017 | 5.0 | 4.3 | 4.7 | 4.1 | 4.1 | 4.1 | 3.9 | 4.2 |

| Ontario FES 2017 | 5.0 | 4.3 | 5.3 | 4.1 | 4.1 | 4.2 | – | 4.4 |

| Current FAO Consensus ** | 5.0 | 4.3 | 5.5 | 4.0 | 4.1 | 4.5 | 3.5 | 4.5 |

| Labour Income | ||||||||

| FAO – Fall 2017 | 4.6 | 3.4 | 4.0 | 4.5 | 4.3 | 4.1 | 3.8 | 4.2 |

| Ontario FES 2017 *** | 4.6 | 3.4 | 4.3 | 4.7 | 4.8 | 4.4 | – | 4.5 |

| Corporate Profits | ||||||||

| FAO – Fall 2017 | 7.1 | 7.3 | 11.7 | 2.2 | 3.7 | 4.4 | 4.4 | 5.4 |

| Ontario FES 2017 | 7.1 | 7.3 | 16.1 | 2.9 | 2.8 | 3.7 | – | 7.1 |

| Household Consumption | ||||||||

| FAO – Fall 2017 | 4.1 | 4.2 | 4.7 | 4.2 | 4.1 | 3.9 | 3.8 | 4.2 |

| Ontario FES 2017 **** | 4.1 | 4.2 | 5.1 | 4.3 | 4.3 | 4.3 | – | 4.5 |

| (Per Cent Growth) | 2015a | 2016a | 2017f | 2018f | 2019f | 2020f | 2021f | Average* |

|---|---|---|---|---|---|---|---|---|

| Real GDP | ||||||||

| FAO – Fall 2017 | 2.9 | 2.6 | 2.8 | 2.1 | 2.0 | 1.9 | 1.9 | 2.2 |

| Ontario FES 2017 | 2.9 | 2.6 | 2.8 | 2.1 | 2.0 | 2.0 | – | 2.2 |

| Current FAO Consensus ** | 2.9 | 2.6 | 2.9 | 2.0 | 2.1 | 2.3 | 2.0 | 2.3 |

| Real GDP Components | ||||||||

| Household Consumption *** | 2.9 | 2.9 | 3.6 | 2.4 | 1.9 | 1.8 | 1.8 | 2.4 |

| Residential Investment | 7.7 | 7.5 | 5.3 | -1.0 | 0.0 | 1.8 | 2.3 | 1.5 |

| Business Investment **** | 7.5 | -8.8 | 2.4 | 4.6 | 4.4 | 4.0 | 3.5 | 3.8 |

| Government (Consumption and Investment) | 1.7 | 2.1 | 1.9 | 1.9 | 1.6 | 1.5 | 1.3 | 1.7 |

| Exports | 3.3 | 2.5 | 0.2 | 2.2 | 2.0 | 2.0 | 2.0 | 1.6 |

| Imports | 3.2 | 0.0 | 2.0 | 2.0 | 1.8 | 1.8 | 1.8 | 1.9 |

| 2015a | 2016a | 2017f | 2018f | 2019f | 2020f | 2021f | |

|---|---|---|---|---|---|---|---|

| Employment (Per Cent Growth) | |||||||

| FAO – Fall 2017 | 0.7 | 1.1 | 1.6 | 1.1 | 1.0 | 0.9 | 0.9 |

| Ontario FES 2017 | 0.7 | 1.1 | 1.4 | 1.1 | 1.1 | 1.0 | – |

| Unemployment Rate (Per Cent) | |||||||

| FAO – Fall 2017 | 6.8 | 6.5 | 6.2 | 6.1 | 6.1 | 6.1 | 6.0 |

| Ontario FES 2017 | 6.8 | 6.5 | 6.2 | 6.2 | 6.1 | 6.1 | – |

| Labour Force (Per Cent Growth) | |||||||

| FAO – Fall 2017 | 0.1 | 0.9 | 1.1 | 1.1 | 1.0 | 0.9 | 0.9 |

| Ontario FES 2017 | – | – | – | – | – | – | – |

| Population Growth (Per Cent) | |||||||

| FAO – Fall 2017 | 0.8 | 1.3 | 1.5 | 1.2 | 1.1 | 1.1 | 1.1 |

| Ontario FES 2017 | – | – | – | – | – | – | – |

| CPI Inflation (Per Cent Growth) | |||||||

| FAO – Fall 2017 | 1.2 | 1.8 | 1.6 | 2.0 | 2.2 | 2.0 | 2.0 |

| Ontario FES 2017 | 1.2 | 1.8 | 1.7 | 2.0 | 2.0 | 2.0 | – |

| Canada Real GDP (Per Cent Growth) | |||||||

| FAO – Fall 2017 | 0.9 | 1.5 | 3.1 | 2.1 | 2.0 | 2.0 | 2.0 |

| Ontario FES 2017 | – | – | – | – | – | – | – |

| U.S. Real GDP (Per Cent Growth) | |||||||

| FAO – Fall 2017 | 2.9 | 1.5 | 2.2 | 2.2 | 2.0 | 1.9 | 1.9 |

| Ontario FES 2017 | 2.9 | 1.5 | 2.2 | 2.4 | 2.1 | 2.1 | – |

| Canadian Dollar (Cents US) | |||||||

| FAO – Fall 2017 | 78.2 | 75.4 | 77.9 | 78.5 | 79.2 | 80.1 | 80.9 |

| Ontario FES 2017 | 78.2 | 75.4 | 77.5 | 81.0 | 81.1 | 81.1 | – |

| WTI Crude Oil (US$) | |||||||

| FAO – Fall 2017 | 49 | 43 | 49 | 52 | 55 | 58 | 61 |

| Ontario FES 2017 | 49 | 43 | 50 | 52 | 56 | 60 | – |

| Three-month Treasury Bill Rate (Per Cent) | |||||||

| FAO – Fall 2017 | 0.5 | 0.5 | 0.7 | 1.5 | 1.9 | 2.3 | 2.6 |

| Ontario FES 2017 | 0.5 | 0.5 | 0.7 | 1.5 | 2.2 | 2.5 | – |

| 10-year Government Bond Rate (Per Cent) | |||||||

| FAO – Fall 2017 | 1.5 | 1.3 | 1.8 | 2.5 | 2.9 | 3.1 | 3.3 |

| Ontario FES 2017 | 1.5 | 1.3 | 1.8 | 2.5 | 3.2 | 3.6 | – |

| ($ Billions) | 2015-16a | 2016-17a | 2017-18f | 2018-19f | 2019-20f | 2020-21f | 2021-22f |

|---|---|---|---|---|---|---|---|

| Revenue | |||||||

| Personal Income Tax | 31.1 | 30.7 | 33.6 | 35.7 | 37.7 | 39.6 | 41.5 |

| Sales Tax | 23.5 | 24.8 | 25.9 | 26.7 | 27.7 | 28.7 | 29.8 |

| Corporations Tax | 11.4 | 14.9 | 14.5 | 14.8 | 15.2 | 15.8 | 16.3 |

| All Other Taxes | 25.8 | 24.1 | 24.7 | 25.5 | 26.4 | 27.3 | 28.2 |

| Total Taxation Revenue | 91.8 | 94.3 | 98.7 | 102.7 | 107.0 | 111.3 | 115.8 |

| Transfers from Government of Canada | 23.1 | 24.5 | 26.2 | 25.5 | 25.0 | 25.8 | 26.6 |

| Income from Government Business Enterprise | 4.9 | 5.6 | 5.1 | 5.9 | 6.2 | 6.5 | 6.7 |

| Other Non-Tax Revenue | 16.3 | 16.3 | 19.4 | 16.5 | 16.6 | 17.3 | 18.0 |

| Total Revenue | 136.1 | 140.7 | 149.4 | 150.7 | 154.8 | 160.8 | 167.0 |

| Expense | |||||||

| Health Sector | 55.0 | 56.0 | 58.0 | 60.5 | 62.5 | 65.4 | 68.9 |

| Education Sector | 26.1 | 26.2 | 27.7 | 28.6 | 29.2 | 30.4 | 31.6 |

| Postsecondary and Training Sector | 9.9 | 10.1 | 10.9 | 11.1 | 11.3 | 11.4 | 11.5 |

| Children’s and Social Services Sector | 15.5 | 16.0 | 16.8 | 17.2 | 17.4 | 17.9 | 18.5 |

| Justice Sector | 4.5 | 4.6 | 4.7 | 4.7 | 4.8 | 5.0 | 5.2 |

| Other Programs | 18.5 | 18.5 | 23.5 | 23.6 | 24.9 | 26.5 | 27.3 |

| Total Program Expense | 129.6 | 131.5 | 141.6 | 145.7 | 150.0 | 156.6 | 163.0 |

| Interest on Debt | 11.6 | 11.7 | 11.8 | 12.1 | 12.6 | 13.2 | 13.8 |

| Total Expense | 141.2 | 143.2 | 153.4 | 157.8 | 162.6 | 169.8 | 176.8 |

| Budget Balance (AG Presentation) |

-5.0 | -2.4 | -4.0 | -7.1 | -7.8 | -9.0 | -9.8 |

| Budget Balance (Government Presentation) |

-3.5 | -1.0 | 0.2 | -1.9 | -1.9 | -2.6 | -3.7 |

| Budget Balance (Ontario FES 2017) |

-3.5 | -1.0 | 0.5 | 0.5 | 0.8 | – | – |

| $ Billions | 2015-16a | 2016-17a | 2017-18f | 2018-19f | 2019-20f | 2020-21f | 2021-22f |

|---|---|---|---|---|---|---|---|

| Budget Balance* | -5.0 | -2.4 | -4.0 | -7.1 | -7.8 | -9.0 | -9.8 |

| Accumulated Deficit | 203.0 | 205.9 | 210.0 | 217.1 | 224.9 | 233.8 | 243.6 |

| Net Debt | 306.4 | 314.1 | 329.2 | 347.7 | 368.0 | 386.8 | 404.4 |

| Change in Net Debt | 7.7 | 15.1 | 18.5 | 20.4 | 18.8 | 17.6 | |

| Net Debt to GDP (Per Cent) |

40.2 | 39.5 | 39.6 | 40.1 | 40.8 | 41.2 | 41.4 |

| FAO Net Debt to GDP (Government Presentation) | |||||||

| Net Debt to GDP (Per Cent) |

38.8 | 37.9 | 37.7 | 38.1 | 38.5 | 38.7 | 38.7 |

Footnotes

[1] See The Fair Hydro Plan: Concerns About Fiscal Transparency, Accountability and Value For Money, Auditor General of Ontario, October 2017; Independent Auditor’s Report, 2016-17 Consolidated Financial Statements, Auditor General of Ontario, 2017; and An Assessment of the Fiscal Impact of the Province’s Fair Hydro Plan, Financial Accountability Office, 2017.

[2] ‘Economic and Fiscal Outlook, Assessing Ontario’s Medium-term Prospects, Spring 2017’, Financial Accountability Office of Ontario.

[3] The FAO’s estimate of net debt incorporates the AG’s recommended accounting framework.

[4] International Monetary Fund, World Economic Outlook, October 2017.

[5] International Monetary Fund, China’s Economic Outlook in Six Charts, August 2017.

[6] The FAO’s forecast incorporates explicit assumptions of higher labour income growth, a small reduction in employment gains and a slight increase in CPI inflation due to the planned increases in Ontario’s minimum wage. See the FAO’s commentary Assessing the Economic Impact of Ontario’s Proposed Minimum Wage Increase for details.

[7] Statistics Canada Annual Household Wealth Distribution Tables (Provisional Data).

[8] The Bank of Canada describes this risk as elevated. Bank of Canada, Financial System Review, June 2017.

[9] Including the Conference Board of Canada, the Centre for Spatial Economics and the Policy and Economic Analysis Program at the University of Toronto.

[10] See The Fair Hydro Plan: Concerns About Fiscal Transparency, Accountability and Value For Money, Auditor General of Ontario, October 2017; Independent Auditor’s Report, 2016-17 Consolidated Financial Statements, Auditor General of Ontario, 2017; and An Assessment of the Fiscal Impact of the Province’s Fair Hydro Plan, Financial Accountability Office, 2017

[11] For details, refer to ‘The Accounting Treatment of Jointly Sponsored Pension Plans’ in the FAO’s Spring 2017 Economic and Fiscal Outlook ’.

[12] See ‘Developments since the FAO’s Spring 2017 Economic and Fiscal Outlook’ in this report’s Appendix.

[13] However, the government’s accounting treatment of net pension assets is consistent with the recommendations from the government’s Independent Pension Asset Expert Advisory Panel. Contrary to the opinion of the Auditor General, the panel’s report concluded that the surpluses in the jointly sponsored pension plans should be fully recognized in the Province’s financial statements.

[14] See Appendix for a detailed comparison of the FAO and the government forecasts.

[15] Some of these temporary revenues – notably proceeds from the sale of carbon allowances or federal transfers for infrastructure – are tied to corresponding spending commitments, which would partially offset the reductions in these revenue sources.

[16] Asset sales include the Province’s 20 per cent sale of Hydro One equity in a secondary offering in 2017-18, which the FAO estimates generated about $0.7 billion in revenue.

[17] The debt retirement charge (DRC) is a charge payable on electricity consumed in Ontario and replaces a portion of debt servicing costs previously included as part of electricity bills before the restructuring of the former Ontario Hydro. The government ended the DRC on residential bills as of January 1, 2016. The DRC will remain on non-residential electricity users’ bills until March 31, 2018.

[18] In the 2017-18 fiscal year, Ontario will hold five carbon market auctions. Going forward, the Province expects to generally hold four auctions each year.

[19] Based on information provided by the Ministry of Finance, the FAO’s projection for ‘Other Spending’ includes $2.3 billion in 2017-18 for a valuation allowance on jointly-sponsored pension assets, growing to $2.9 billion by 2021-22. In addition, the FAO includes expenses related to the electricity cost refinancing portion of the FHP, which average $2.8 billion per year over the outlook.

[20] In the 2017 FES, the government announced new funding for additional spending for small businesses, seniors and child care. However, the additional expenses for child care is fiscally neutral since it is funded by a corresponding increase in federal transfer revenue.

[21] On the government’s accounting basis, which excludes the impact of the pension adjustment and the electricity cost refinancing portion of the FHP.

[22] The FAO’s estimate of net debt reflects the Auditor General’s recommended accounting framework.