Summary

- The Government of Ontario’s (the Province’s) debt is rated by four principal international credit rating agencies,[1] based on their assessments of Ontario’s economic and financial outlook, and future risks. These credit ratings represent the agencies’ opinions on the Province’s ability to meet its debt-related financial obligations.

- After dramatic improvements in Ontario’s finances stemming from a post-pandemic surge in economic activity, the four credit rating agencies have all recently reaffirmed their ratings for the Province in updated assessments and maintained the outlook as stable. In general, the agencies continue to rate Ontario as an “extremely strong,” investment-grade borrower.

- The credit rating agencies indicate that Ontario’s strong credit rating is supported by its large and diversified economy, high liquidity and prudent debt management program. As well, Canada’s federal-provincial framework provides provinces with the flexibility to adjust both tax policy and program spending, in addition to continued and predictable federal transfers.

- All credit rating agencies indicated that continued fiscal improvement, in the form of declining budget deficits and a falling debt burden, could lead to a positive ratings action (either a rating upgrade or positive outlook). Conversely, rising deficits and an increasing debt burden could lead to a negative rating action (a rating downgrade or negative outlook).

- Since the FAO’s previous credit rating note, only Alberta saw its rating change, when it was upgraded by S&P. As a result, Alberta’s average credit rating moved up to tie Ontario as the fifth highest rated province.

Ontario’s Credit Rating Reaffirmed

When the FAO released its last credit rating report in September 2021, Ontario's 2021 budget projected deficits of $38.5 billion in 2020-21 and $33.1 billion in 2021-22, and significant increases in the Province’s debt burden. Despite the projected fiscal deterioration in the 2021 budget, all four credit rating agencies maintained the Province’s credit rating and outlook in their 2021 assessments.

Since then, Ontario has released its Public Accounts for both 2020-21 and 2021-22, which showed dramatic improvements in the Province’s finances. For 2020-21, Ontario recorded a deficit of $16.4 billion (+$22.1 billion improvement compared to the 2021 budget outlook) and a surplus of $2.1 billion in 2021-22 (+$35.2 billion improvement).

Following this progress in the Province’s fiscal results and the improved outlook presented in the 2022 Ontario Economic Outlook and Fiscal Review, all four credit rating agencies have released credit rating updates for Ontario, each reaffirming Ontario’s credit rating and outlook.

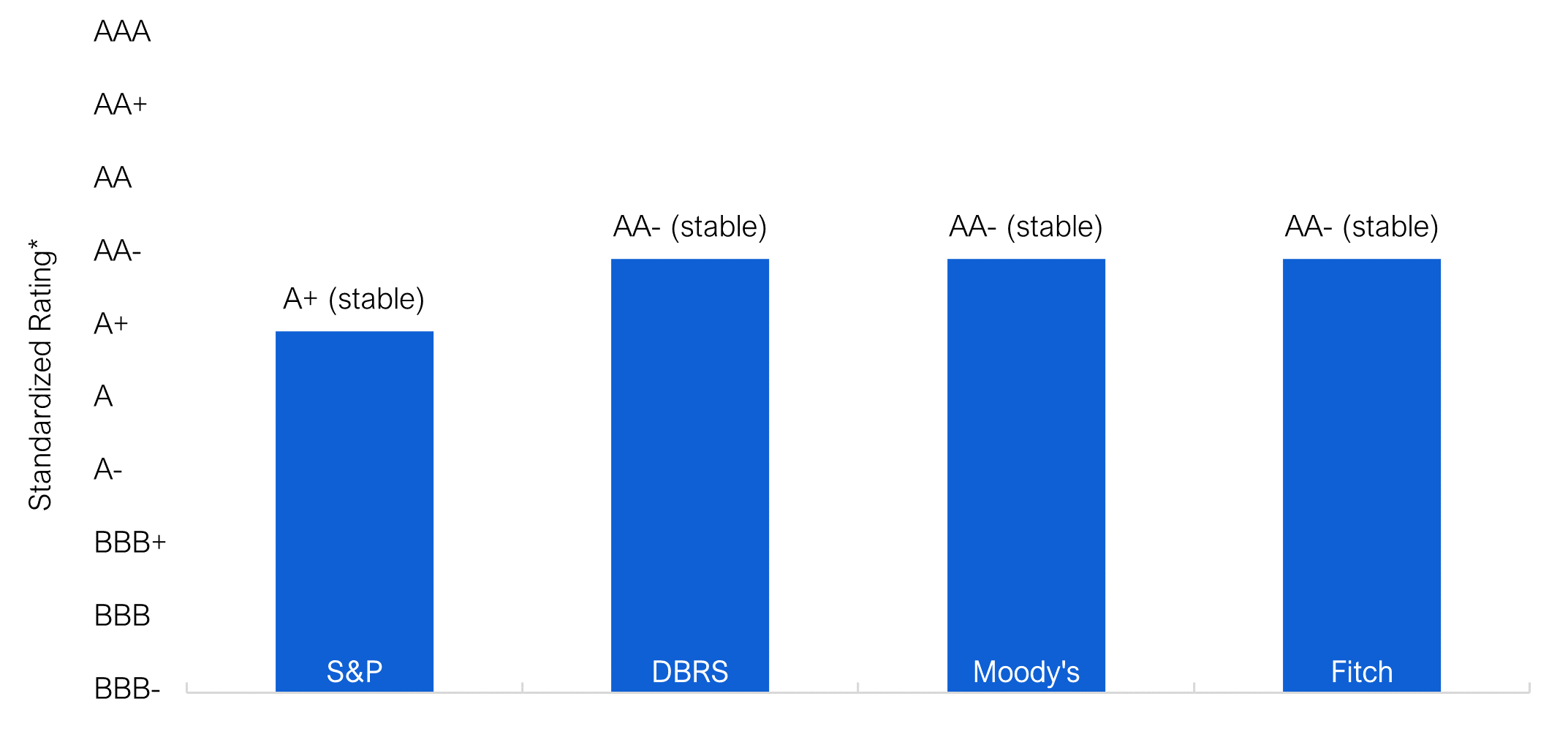

Figure 1 Ontario's credit ratings reaffirmed by all rating agencies

* See Table 2 for rating conversion table.

Source: S&P, DBRS, Fitch, Moody’s, and FAO.

Based on a standardized scale,[2] Ontario’s debt is currently rated AA- (extremely strong, investment-grade borrower - fourth highest rating) by three of the four credit rating agencies and A+ (very strong, investment-grade borrower - fifth highest rating) by S&P. All credit rating agencies affirmed that Ontario’s credit outlook remains stable, indicating a low likelihood of a rating change over the medium term.

Ontario’s credit rating and outlook are based on the agencies’ expectations that after returning to a budget deficit in 2022-23, the Province's deficits will continue to improve over the outlook despite slowing economic growth in 2023 and a modest recovery in 2024. This improvement will limit the rise in the debt burden, even with the high capital spending included from the Province’s capital program. At the same time, despite rising interest rates, the Province’s interest burden is expected to remain relatively stable over the outlook.

The credit rating agencies highlighted both positive and negative factors that contributed to Ontario’s rating and outlook.

Positive factors

Credit rating agencies indicated that Ontario’s strong credit rating is supported by the Province’s large and diversified economy, high liquidity and prudent debt management program. As well, Canada’s federal-provincial framework provides provinces with the flexibility to adjust both tax policy and program spending, in addition to continued and predictable federal transfers.

Economy

The Province has a large and diversified economy, which includes both manufacturing and services sectors, as well as strong trade relationships throughout North America and globally. The Province’s economy also benefits from its favourable demographics and wealth factors, including its high net international in-migration and its high GDP per capita. These factors contribute to reliable revenue generation, even in unstable times, which Moody’s highlighted was evidenced by the resilience in revenues in 2021-22 following the disruptions from the COVID-19 pandemic.

Liquidity and debt management

The Province maintains large liquid reserves to ensure it can meet its short-term obligations in periods of financial market stress. The Province also has strong access to both domestic and international borrowing markets, even in times of market turmoil, and a prudent debt management program, which seeks to limit the impact of risks related to refinancing, changes in interest rates and exchange rate fluctuations on its debt.[3]

Federal-provincial framework

Ontario, like other provinces, has considerable fiscal flexibility to adjust both tax policy[4] and program spending, giving it the ability to raise revenues or decrease spending to meet fiscal challenges. The federal-provincial relationship also means the Province receives predictable transfers from the federal government, which supplement own-source revenues (such as revenue from taxation, government business enterprises or other non-tax revenue). The credit rating agencies also regard the high likelihood of extraordinary support from the federal government in the event of a crisis as having a positive impact on Ontario’s rating.[5]

Negative factors

The agencies also identified challenges that negatively impact Ontario’s credit rating, including the Province’s elevated debt burden, macroeconomic conditions and policy pressures.

Debt burden

Ontario’s debt burden, which measures debt as a share of GDP or revenues, is high relative to both domestic and international peers. The Province’s debt burden has increased since the 2008-2009 recession, the result of continuous deficits, which were further exacerbated by the pandemic. Although debt service costs are expected to remain relatively stable over the outlook, Ontario’s high debt burden means if interest rates rise by more than expected or remain higher for longer, the Province may face greater budgetary pressure.

Macroeconomic conditions

While the Province is forecasting a slowdown in economic growth in 2023, followed by a modest recovery in 2024, several agencies warned that both domestic and global macroeconomic conditions may negatively impact fiscal results. The impacts of high inflation, rising interest rates, declining housing market activity, slowing global trade and the ongoing Russian war in Ukraine may be worse than anticipated, resulting in weaker economic activity, reducing revenues or increasing spending beyond what is projected in the fiscal plan.

Policy pressures

The government may face spending pressures as it seeks to address concerns brought forward during the pandemic, including issues related to long-term care, the lack of paid sick days for lower-income workers and the backlog of surgeries in the health sector. Upcoming collective bargaining agreements may also result in greater spending as workers seek higher wage increases. While S&P indicated the government has a good track record of meeting deficit targets, Moody’s[6] noted that the Province may underestimate the costs to resolve these pressures.

Potential rating changes

The credit rating agencies indicated that continued fiscal improvement, in the form of declining budget deficits and a falling debt burden could lead to a positive ratings action (either a rating upgrade or positive outlook). Conversely, rising deficits and an increasing debt burden could lead to a negative rating action (a rating downgrade or negative outlook).

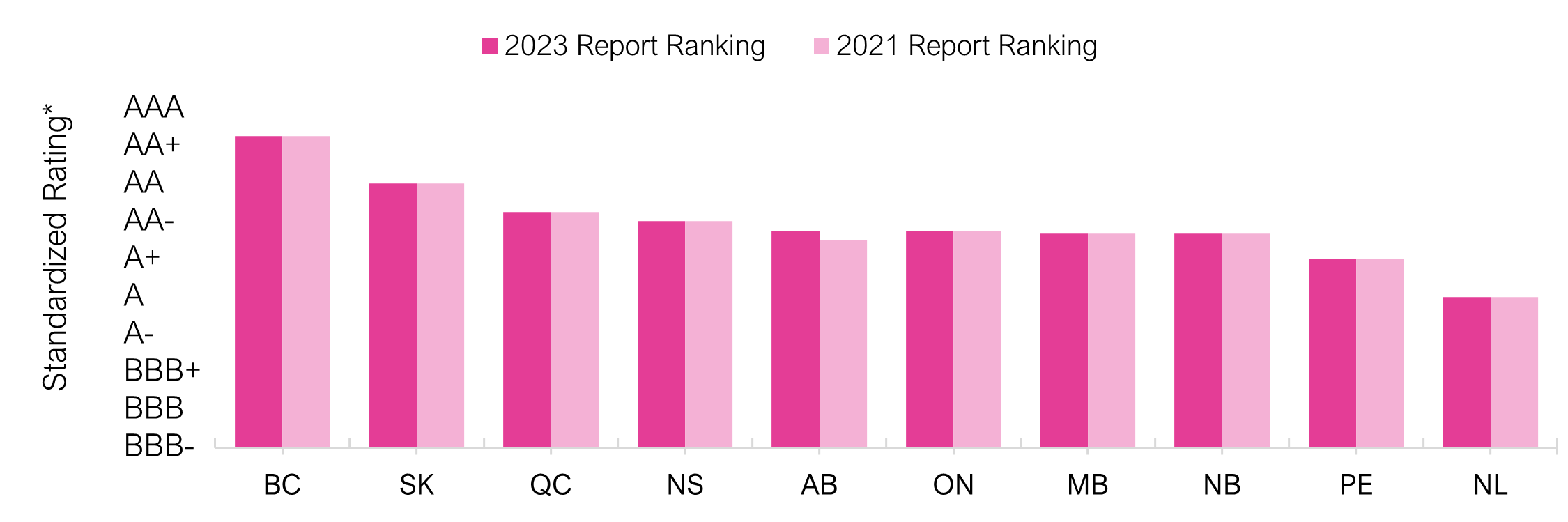

Ontario’s rating relative to other provinces remains stable

Since the last credit rating update published by the FAO in September 2021, only Alberta saw a change in its credit rating, which was upgraded by S&P. The rating upgrade increased Alberta’s average credit rating, moving it up to tie Ontario as the fifth highest rated province. Three provinces – Alberta, New Brunswick, and Newfoundland and Labrador – saw upgrades to their outlook.

Figure 2 Provincial credit ratings unchanged since 2021 report apart from Alberta

* See Table 2 for rating conversion table.

Source: DBRS, Fitch, Moody’s, S&P and FAO.

All rating and outlook upgrades reflected the impact of improved fiscal performance on stabilizing the medium-term debt burden below key thresholds for the affected provinces.

- Alberta was upgraded by S&P[7] from A to A+ in May 2022, while Moody’s[8] and DBRS[9] revised Alberta’s outlook from stable to positive in April 2022 and September 2022, respectively. These changes reflected the improvement of Alberta’s budget and debt outlook attributed to its strong economic recovery and surging oil prices.

- New Brunswick’s outlook was revised from stable to positive by Moody’s[10] in July 2022. This change in outlook was based on Moody’s forecast that if New Brunswick achieves its budget plan, modest budget surpluses and stable capital spending could lower and then stabilize its debt burden.

- Newfoundland and Labrador’s outlook was revised from negative to stable by DBRS[11] (September 2021), S&P[12] (July 2022) and Moody’s[13] (July 2022). As rationale for the revision, S&P noted the fiscal gains brought by high oil prices coinciding with prudent financial management, while DBRS and Moody’s noted the impact of lower deficits in stabilizing the debt burden and the agreement signed with the federal government which will reduce the risk that Newfoundland and Labrador will need to support the Muskrat Falls electricity generation project.

Appendix

| Province | S&P | DBRS | Moody’s | Fitch | Average Rating (1 = highest rating) |

|---|---|---|---|---|---|

| British Columbia | AA+ (stable) | AA high (stable) | Aaa (stable) | AA+ (stable) | 1.75 |

| Alberta | A+ (stable) | AA low (positive) | Aa3 (positive) | AA- (stable) | 4.25 |

| Saskatchewan | AA (stable) | AA low (stable) | Aa1 (stable) | AA (stable) | 3.00 |

| Manitoba | A+ (stable) | A high (stable) | Aa2 (stable) | 4.33 | |

| Ontario | A+ (stable) | AA low (stable) | Aa3 (stable) | AA- (stable) | 4.25 |

| Quebec | AA- (stable) | AA low (stable) | Aa2 (stable) | AA- (stable) | 3.75 |

| New Brunswick | A+ (stable) | A high (stable) | Aa2 (positive) | 4.33 | |

| Nova Scotia | AA- (stable) | A high (stable) | Aa2 (stable) | 4.00 | |

| Newfoundland & Labrador | A (stable) | A low (stable) | A1 (stable) | 6.00 | |

| Prince Edward Island | A (stable) | A (stable) | Aa2 (stable) | 5.00 |

| Rating Description | Credit Quality | S&P | DBRS | Moody’s | Fitch | |

|---|---|---|---|---|---|---|

| Long Term | Long Term | Long Term | Long Term | Ranking | ||

| Investment-grade | Extremely Strong | AAA | AAA | Aaa | AAA | 1 |

| AA+ | AA high | Aa1 | AA+ | 2 | ||

| AA | AA | Aa2 | AA | 3 | ||

| AA- | AA low | Aa3 | AA- | 4 | ||

| Very Strong | A+ | A high | A1 | A+ | 5 | |

| A | A | A2 | A | 6 | ||

| A- | A low | A3 | A- | 7 | ||

| Strong | BBB+ | BBB high | Baa1 | BBB+ | 8 | |

| BBB | BBB | Baa2 | BBB | 9 | ||

| BBB- | BBB low | Baa3 | BBB- | 10 | ||

| Non-investment-grade | Speculative | BB+ | BB high | Ba1 | BB+ | 11 |

| BB | BB | Ba2 | BB | 12 | ||

| BB- | BB low | Ba3 | BB- | 13 | ||

| B+ | B high | B1 | B+ | 14 | ||

| B | B | B2 | B | 15 | ||

| B- | B low | B3 | B- | 16 | ||

| CCC | CCC | Caa | CCC | 17 |

Graphical Descriptions

| Credit Rating Agency | Standardized Rating* |

|---|---|

| S&P | A+ (stable) |

| DBRS | AA- (stable) |

| Moody's | AA- (stable) |

| Fitch | AA- (stable) |

| Province | 2023 Report Ranking | 2021 Report Ranking |

|---|---|---|

| BC | 1.75 | 1.75 |

| SK | 3.00 | 3.00 |

| QC | 3.75 | 3.75 |

| NS | 4.00 | 4.00 |

| AB | 4.25 | 4.50 |

| ON | 4.25 | 4.25 |

| MB | 4.33 | 4.33 |

| NB | 4.33 | 4.33 |

| PE | 5.00 | 5.00 |

| NL | 6.00 | 6.00 |

Footnotes

[1] The four credit rating agencies are Moody’s Investors Service (Moody’s), S&P Global Ratings (S&P), DBRS Limited (DBRS) and Fitch Ratings (Fitch). The agencies continually review the province’s credit rating and typically publish an update on their view of the Province’s finances and credit quality annually, based on the government’s latest financial reports or statements and their view of the outlook and risks.

[2] See Table 2: The Agencies’ Credit Rating Scales in the Appendix for the scale used by each credit rating agency. The FAO’s standardized rating scale is based on the rating classifications used by S&P and Fitch.

[3] Refinancing risk is the risk that a borrower will not be able to borrow to repay existing debt. Interest rate risk is the risk that movements in interest rates will increase debt servicing costs. Exchange rate risk is the risk that movements in exchange rates of foreign denominated debt will increase debt servicing costs. For details on how Ontario manages these risks see Ontario Financing Authority’s Risk Management.

[4] DBRS highlighted the Province’s lower relative revenue per capita compared to other provinces, which may give the government room to increase tax rates, if necessary.

[5] This support was evidenced during the pandemic when the federal government provided funding to governments, individuals, and business, limiting the extent of provincial fiscal deterioration caused by the COVID-19 pandemic. Similarly, the Bank of Canada established provincial debt buying programs to ensure liquidity in provincial bond markets. For more information, see S&P’s Institutional Framework Assessment: Canadian Provinces.

[6] Moody’s also noted potential policy pressures the Province may face to alleviate pressures on households from the high cost of living, either by reducing taxes (i.e. the recent extension in the temporary fuel and gas tax cut) or increasing program spending (i.e. the electricity subsidization program introduced by previous governments and enhanced in recent years).

[7] See S&P’s Alberta Research Update for more details.

[8] See Moody’s Alberta Rating Action for more details.

[9] See DBRS’ Alberta Rating Action Press Release for more details.

[10] See Moody’s New Brunswick Rating Action for more details.

[11] See DBRS’ Newfoundland and Labrador Press Release for more details.

[12] See S&P’s Province of Newfoundland and Labrador Outlook Revised To Stable From Negative; 'A' Rating Affirmed for more details.

[13] See Moody’s Newfoundland and Labrador Rating Action for more details.